Most Popular

![[Grace Kao] Hybe vs. Ador: Inspiration, imitation and plagiarism](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/28/20240428050220_0.jpg&u=)

![[Herald Interview] Mom’s Touch seeks to replicate success in Japan](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/29/20240429050568_0.jpg&u=)

-

6

Police to open alleged stalking probe over pastor over Dior bag scandal

-

7

'Queen of Tears' finale sets record viewership ratings as tvN's most-watched series ending

-

8

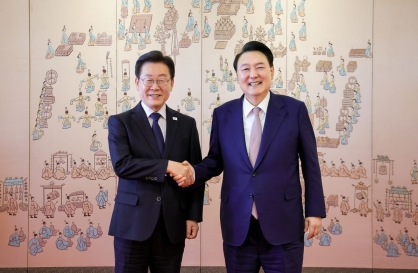

[News Focus] Lee tells Yoon that he has governed without political dialogue

![[News Focus] Lee tells Yoon that he has governed without political dialogue](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/29/20240429050696_0.jpg&u=20240429210658)

-

9

Seoul to deploy more military doctors to fill med prof void

-

10

Liberal bloc moves to rewrite student rights ordinance

![[News Focus] Lee tells Yoon that he has governed without political dialogue](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/29/20240429050696_0.jpg&u=20240429210658)

[Christopher Balding] Is China really deleveraging?

By Korea HeraldPublished : May 15, 2017 - 17:46

There’s growing evidence that China is finally scaling back its epic borrowing binge. That’s important for a lot of reasons, not least for reducing risk and avoiding a financial crisis. The question is whether the government can sustain the pain.

Regulators in Beijing are well aware of the risks that excessive leverage poses, and have tried many times over the years to crack down. Yet they routinely fail to rein in local government officials who get promoted by boosting economic growth, regardless of what systemic risks they may be incurring by binging on debt. To adapt a Chinese proverb: Growth is high and the banking regulator is far away.

Evidence is mounting that this time is different. Lending to banks from the People’s Bank of China, which surged by 243 percent from December 2015 to January 2017, has declined by 12 percent in the past two months. Loans to non-financial corporations are up a relatively moderate 7.3 percent from March 2016, which is a slower rate than nominal growth in gross domestic product. Although this clampdown followed an enormous surge of credit in the first half of last year, it does suggest real progress.

Another good sign is that the government is starting to rein in shadow banking. Issuance of risky wealth-management products declined by 18 percent in April from March, as banks and insurance companies have been pressured to rely on them less. Because the sector is so enormous -- with more than $4 trillion outstanding -- getting it under control is a crucial prerequisite for any serious deleveraging.

Predictably, though, these reforms have pushed down asset prices. Stocks, bonds, commodities and real estate have all turned strongly negative. Interest rates have been inching up, inflicting losses on bond investors. Allocations of stocks and commodities in wealth-management products are at their lowest levels in almost a year, depressing prices further.

This will probably get worse. Industrial capacity is widely up while demand growth is flat. Steel rebar prices have dropped by only 8 percent from their highs this year, and remain up by an amazing 91 percent since December 2015. Yet even this small dip has had a major effect. In March, when prices peaked, 85 percent of Hebei steelmakers reported being profitable. Now that figure stands at 66 percent.

If an 8 percent drop in prices results in a 19 percentage point decline in the number of profitable steel mills, more serious price drops could well push the industry to the brink. For a sector in which listed firms have suffered operational losses of 5.1 billion yuan ($739 million) since 2010 -- during one of the largest building booms the world has ever seen -- a sustained deleveraging effort may well spell disaster.

The property market could also be in for a rough ride. Chinese consumers take the ability to buy an apartment as a birthright, and prices have risen in response to demand. Mortgage lending has grown by 31 percent since March 2016. But as cities place more restrictions on purchases and banking regulators get tougher about slowing mortgage growth, the resulting pressure on prices could be an unpleasant surprise for homeowners and indebted developers.

Making matters worse, rising bond yields are making it harder for heavily indebted firms to meet their obligations. Although this hasn’t yet started to push companies over the edge, the longer borrowing costs are elevated in a highly indebted economy, the more risks accumulate. Regulators should be prepared for more bankruptcies and more nonperforming loans.

For now, China’s government seems willing to accept all this as the price of reducing financial risk. And that’s commendable. But as the pain gets worse -- and spreads to state-owned companies, consumers and banks -- the pressure will only build to once again let credit balloon. Economics is the study of trade-offs. Beijing will soon have to decide whether this one is worth it.

By Christopher Balding

Christopher Balding is an associate professor of business and economics at the HSBC Business School in Shenzhen, China. -- Ed.

(Bloomberg)

Regulators in Beijing are well aware of the risks that excessive leverage poses, and have tried many times over the years to crack down. Yet they routinely fail to rein in local government officials who get promoted by boosting economic growth, regardless of what systemic risks they may be incurring by binging on debt. To adapt a Chinese proverb: Growth is high and the banking regulator is far away.

Evidence is mounting that this time is different. Lending to banks from the People’s Bank of China, which surged by 243 percent from December 2015 to January 2017, has declined by 12 percent in the past two months. Loans to non-financial corporations are up a relatively moderate 7.3 percent from March 2016, which is a slower rate than nominal growth in gross domestic product. Although this clampdown followed an enormous surge of credit in the first half of last year, it does suggest real progress.

Another good sign is that the government is starting to rein in shadow banking. Issuance of risky wealth-management products declined by 18 percent in April from March, as banks and insurance companies have been pressured to rely on them less. Because the sector is so enormous -- with more than $4 trillion outstanding -- getting it under control is a crucial prerequisite for any serious deleveraging.

Predictably, though, these reforms have pushed down asset prices. Stocks, bonds, commodities and real estate have all turned strongly negative. Interest rates have been inching up, inflicting losses on bond investors. Allocations of stocks and commodities in wealth-management products are at their lowest levels in almost a year, depressing prices further.

This will probably get worse. Industrial capacity is widely up while demand growth is flat. Steel rebar prices have dropped by only 8 percent from their highs this year, and remain up by an amazing 91 percent since December 2015. Yet even this small dip has had a major effect. In March, when prices peaked, 85 percent of Hebei steelmakers reported being profitable. Now that figure stands at 66 percent.

If an 8 percent drop in prices results in a 19 percentage point decline in the number of profitable steel mills, more serious price drops could well push the industry to the brink. For a sector in which listed firms have suffered operational losses of 5.1 billion yuan ($739 million) since 2010 -- during one of the largest building booms the world has ever seen -- a sustained deleveraging effort may well spell disaster.

The property market could also be in for a rough ride. Chinese consumers take the ability to buy an apartment as a birthright, and prices have risen in response to demand. Mortgage lending has grown by 31 percent since March 2016. But as cities place more restrictions on purchases and banking regulators get tougher about slowing mortgage growth, the resulting pressure on prices could be an unpleasant surprise for homeowners and indebted developers.

Making matters worse, rising bond yields are making it harder for heavily indebted firms to meet their obligations. Although this hasn’t yet started to push companies over the edge, the longer borrowing costs are elevated in a highly indebted economy, the more risks accumulate. Regulators should be prepared for more bankruptcies and more nonperforming loans.

For now, China’s government seems willing to accept all this as the price of reducing financial risk. And that’s commendable. But as the pain gets worse -- and spreads to state-owned companies, consumers and banks -- the pressure will only build to once again let credit balloon. Economics is the study of trade-offs. Beijing will soon have to decide whether this one is worth it.

By Christopher Balding

Christopher Balding is an associate professor of business and economics at the HSBC Business School in Shenzhen, China. -- Ed.

(Bloomberg)

-

Articles by Korea Herald

![[Today’s K-pop] Seventeen sets sales record with best-of album](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=642&simg=/content/image/2024/04/30/20240430050818_0.jpg&u=)