Most Popular

-

1

Ador CEO denies allegations, accuses Hybe of mistreating NewJeans

-

2

[Herald Interview] 'Amid aging population, Korea to invite more young professionals from overseas'

![[Herald Interview] 'Amid aging population, Korea to invite more young professionals from overseas'](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/24/20240424050844_0.jpg&u=20240424200058)

-

3

Nicaragua shuts down Seoul embassy

-

4

Medical reform committee kicks off despite boycott from doctors

-

5

10-man S. Korea lose to Indonesia to miss out on Paris Olympic football qualification

![[Herald Interview] 'Amid aging population, Korea to invite more young professionals from overseas'](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/24/20240424050844_0.jpg&u=20240424200058)

-

6

Rocket engine expert, ex-NASA exec to lead Korea's new space agency

-

7

SK hynix pledges W20tr to ramp up DRAM production at home

-

8

DP leader says he will meet Yoon without conditions

-

9

Over 9,000 hotline calls made by stalking victims in 2023

-

10

[Hello India] Hyundai Motor vows to boost 'clean mobility' in India

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

Worrisome signs are resurfacing from the issue of red-hot credit card competition, reminiscent of the 2003 bad debt fiasco, prompting regulators to consider fresh restrictions.

Major card issuers have been fighting a marketing war since last year, vying for a bigger slice of consumer spending as it gets on track to recovery.

The competition led to sharp increases in card issuances and service loans, similar to the last industry crisis, in which the then-largest issuer LG Card and several others had to be rescued with creditors’ money.

The trend is more risky coming on top of already high household debt, experts said.

The average number of cards held by a Korean adult reached 4.59 last September, exceeding the former record-high of 4.57 in early 2003, according to the Credit Finance Association.

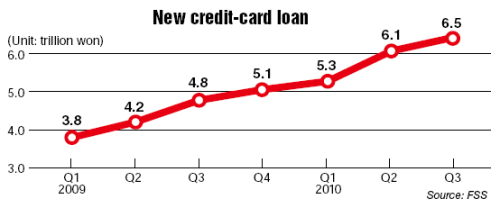

Combined card loans have continued to surge over the past two years, according to the Financial Services Commission.

While these loans reached 3.8 trillion won ($3.3 billion) at the end of March 2009, the figure increased by 39.5 percent to 5.3 trillion won at the end of March 2010. And it jumped further to 6.5 trillion won at the end of September 2010.

The number of card salespeople has steadily increased thanks to eased regulations and fiercer competition.

The number dropped sharply to below 20,000 in 2004 from 87,700 in 2002, in the aftermath of the 2003 woes. But it rose again to reach 50,000 in 2010.

Experts are concerned about a flood of defaults stemming from card holdings by people with low-level credit standings.

“Bad loan risk may begin among those who usually use card loans and cash advance services,” an economist at the Korea Institute of Finance said.

He said growing concerns in the market involve households’ spiraling interest burden as the Bank of Korea is moving to raise its benchmark rate further this year.

In January, the central bank unexpectedly raised the key interest rate by a quarter percentage point to 2.75 percent amid mounting inflationary pressure. It marked the third rate increase since the onset of the global financial crisis.

Regulatory officials downplayed the possibility of another round of credit card crises but did not rule out potential risks.

Financial Supervisory Service director general Nam Myung-seob said late last month that the average credit delinquency ratio among card companies stays safe, currently at 1 percent.

But he said, “(A) worrisome situation is the continuous growth in card loans and fierce marketing competition among issuers.”

The financial authority has begun to map out stern measures to crack down on reckless card issuance.

“We will announce a comprehensive measure for effective risk management for the credit card sector,” an FSC official said.

Competition among card issuers began to heat up in the second half of 2010.

Five major card issuers ― Shinhan, Samsung, Hyundai, Lotte and Hana SK ― spent 1.37 trillion won for their promotion and marketing during the first three quarters of 2010, including 584.7 billion won in the July-to-September period.

This year newcomers are set to fight uphill battles against the five companies. The FSS has endorsed Kookmin Bank’s spin-off of its credit card unit as an independent business entity.

In addition, Woori Bank, Citibank Korea, the National Agricultural Cooperative Federation and Korea Exchange Bank are also said to be mulling spin-offs.

The state-controlled Korea Development Bank and Korea Post are reportedly considering tapping the lucrative card business.

By Kim Yon-se (kys@heraldcorp.com)

Major card issuers have been fighting a marketing war since last year, vying for a bigger slice of consumer spending as it gets on track to recovery.

The competition led to sharp increases in card issuances and service loans, similar to the last industry crisis, in which the then-largest issuer LG Card and several others had to be rescued with creditors’ money.

The trend is more risky coming on top of already high household debt, experts said.

The average number of cards held by a Korean adult reached 4.59 last September, exceeding the former record-high of 4.57 in early 2003, according to the Credit Finance Association.

Combined card loans have continued to surge over the past two years, according to the Financial Services Commission.

While these loans reached 3.8 trillion won ($3.3 billion) at the end of March 2009, the figure increased by 39.5 percent to 5.3 trillion won at the end of March 2010. And it jumped further to 6.5 trillion won at the end of September 2010.

The number of card salespeople has steadily increased thanks to eased regulations and fiercer competition.

The number dropped sharply to below 20,000 in 2004 from 87,700 in 2002, in the aftermath of the 2003 woes. But it rose again to reach 50,000 in 2010.

Experts are concerned about a flood of defaults stemming from card holdings by people with low-level credit standings.

“Bad loan risk may begin among those who usually use card loans and cash advance services,” an economist at the Korea Institute of Finance said.

He said growing concerns in the market involve households’ spiraling interest burden as the Bank of Korea is moving to raise its benchmark rate further this year.

In January, the central bank unexpectedly raised the key interest rate by a quarter percentage point to 2.75 percent amid mounting inflationary pressure. It marked the third rate increase since the onset of the global financial crisis.

Regulatory officials downplayed the possibility of another round of credit card crises but did not rule out potential risks.

Financial Supervisory Service director general Nam Myung-seob said late last month that the average credit delinquency ratio among card companies stays safe, currently at 1 percent.

But he said, “(A) worrisome situation is the continuous growth in card loans and fierce marketing competition among issuers.”

The financial authority has begun to map out stern measures to crack down on reckless card issuance.

“We will announce a comprehensive measure for effective risk management for the credit card sector,” an FSC official said.

Competition among card issuers began to heat up in the second half of 2010.

Five major card issuers ― Shinhan, Samsung, Hyundai, Lotte and Hana SK ― spent 1.37 trillion won for their promotion and marketing during the first three quarters of 2010, including 584.7 billion won in the July-to-September period.

This year newcomers are set to fight uphill battles against the five companies. The FSS has endorsed Kookmin Bank’s spin-off of its credit card unit as an independent business entity.

In addition, Woori Bank, Citibank Korea, the National Agricultural Cooperative Federation and Korea Exchange Bank are also said to be mulling spin-offs.

The state-controlled Korea Development Bank and Korea Post are reportedly considering tapping the lucrative card business.

By Kim Yon-se (kys@heraldcorp.com)

![[Today’s K-pop] NewJeans' single teasers release amid intrigue](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=642&simg=/content/image/2024/04/26/20240426050575_0.jpg&u=)