Most Popular

-

1

40 flights canceled on Jeju Island due to bad weather

-

2

Pandemic left Korea more depressed than before: report

-

3

N. Korea slams US, other countries for seeking alternative to UN sanctions monitoring panel

-

4

Korean labor force to shrink by 10 million by 2044: report

-

5

Gov't appears to shelve punitive measures against mass walkout by doctors

-

6

[AtoZ Korean Mind] Does your job define who you are? Should it?

![[AtoZ Korean Mind] Does your job define who you are? Should it?](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/06/20240506050099_0.jpg&u=)

-

7

Govt. asks hospitals to mitigate impact of medical professors' absence

-

8

S. Korea's working-age population to dip nearly 10m by 2044 amid low births

-

9

Doggy patrol team on the move to protect their cities

-

10

Samsung mocks Apple over iPhone alarm glitch

![[AtoZ Korean Mind] Does your job define who you are? Should it?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/06/20240506050099_0.jpg&u=)

[ANALYST REPORT] Cheil Worldwide: End of uncertainty and start of recovery

By 박한나Published : June 15, 2016 - 13:56

Talks with global advertising agencies end without any agreement

Discussions on cooperation between Cheil Worldwide’s major shareholders and global ad agencies ended without any agreement, according to the Data Analysis, Retrieval and Transfer (DART) System of the Financial Supervisory Service. Publicis and Samsung ended talks for the acquisition of Cheil Worldwide. The company also said that no talks are underway with a third party on the majority stake sale, dismissing rumors about disposal to a Chinese company.

The announcement is compelling as Publicis is the only viable bidder. Long-term uncertainty over the majority stake disposal seems to have mostly been lifted.

Quarterly earnings momentum to continue

Cheil Worldwide is forecast to post 2Q16 consolidated gross profit of W265.1bn (+9.8% YoY) and operating profit of W44.5bn (+5.7% YoY), meeting the consensus (W44.2bn). Operating profit should grow markedly QoQ due to high seasonal demand. Gross profit is expected to rise by W2.5bn each quarter due to the acquisition of Founded (B2B marketing firm established in 2012 in the UK) in April. The deal should boost profits by 1.5%.

Consolidated gross profit and operating profit are projected to grow 10.9% and 20.8% YoY, respectively, to W262.3bn and W32.7bn in 3Q16. Top-line growth should accelerate at home and abroad given the Rio Olympics in August. We expect gross profit to grow 6.6% YoY at the parent company and 12.4% YoY for overseas operations. Both growth and profits should meet expectations.

Retain BUY for target price of W21,000

We retain our BUY rating on Cheil Worldwide for a target price of W21,000, based on a target PER of 24x (10% discount to past 3-year average) for 2016F EPS. We considered slowing ad spending by the major client. The 2016F PER is 18x. Adjusted PER excluding year-end net cash of W420bn is 14x. ROE is forecast to recover to double-digit levels. Considering the dividend payout ratio, there is no reason not to buy the stock. The share price is expected to recover.

Talks on majority stake sale fall through; share price expected to recover

Discussions on cooperation between Cheil Worldwide’s major shareholders and global ad agencies ended without any agreement, according to the DART System of the Financial Supervisory Service. Publicis and Samsung ended talks on the acquisition of Cheil Worldwide. Synergy after the stake sale is important, but long-term marketing strategy of advertisers is the key variable. It seems it was difficult to commit to placing orders for ads for a set period of time regardless of their results. Cheil Worldwide also said that no talks are underway with a third party on the majority stake disposal, dismissing rumors about a stake sale to a Chinese company.

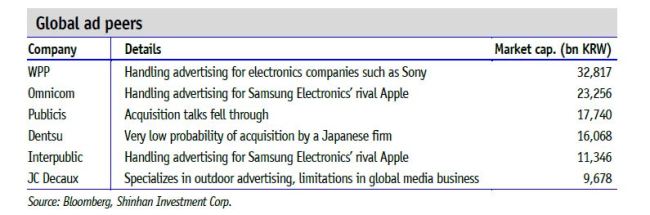

The announcement is compelling as Publicis is the only viable bidder. Long-term uncertainty over the majority stake sale seems to have mostly been lifted. WPP, the world’s largest ad agency, is already working with global electronics companies including Sony. Omnicom and Interpublic are creating ads for Apple. They are unlikely to offer to acquire Cheil Worldwide, even after considering the fact that ad agencies usually work for several brands to win orders from competitors. Considering public sentiment, there is very little possibility of a sale to Dentsu of Japan.

Even based on conservative estimates, the PER has dropped to a low level of 18x based on 2016F EPS. The share price band was W20,000-22,000 before the noise about the sale. The PER excluding estimated net cash at end-2016 (W420bn) is only 14x. The stock has rarely traded below a PER of 20x. The average multiple was 27x over the past three years. Even if a 10-15% discount is applied to the target multiple, the share price should rebound 15-20%. Overseas gross profit, a key share price indicator, is growing steadily.

Source: Shinhan Investment Corp. http://www.shinhaninvest.com/eng/