Most Popular

-

1

40 flights canceled on Jeju Island due to bad weather

-

2

Pandemic left Korea more depressed than before: report

-

3

N. Korea slams US, other countries for seeking alternative to UN sanctions monitoring panel

-

4

Korean labor force to shrink by 10 million by 2044: report

-

5

[AtoZ Korean Mind] Does your job define who you are? Should it?

![[AtoZ Korean Mind] Does your job define who you are? Should it?](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/06/20240506050099_0.jpg&u=)

![[AtoZ Korean Mind] Does your job define who you are? Should it?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/06/20240506050099_0.jpg&u=)

-

6

Gov't appears to shelve punitive measures against mass walkout by doctors

-

7

Govt. asks hospitals to mitigate impact of medical professors' absence

-

8

Allegations surrounding BTS resurface, enraged fans demand apology

-

9

S. Korea's working-age population to dip nearly 10m by 2044 amid low births

-

10

Doggy patrol team on the move to protect their cities

Following is the seventh and last in a series of articles on the prospects for the world economy in 2015. ― Ed.

While bilateral free trade agreements, as a means to further the market-opening and rule-making agenda, have been globally picking up steam, there have also been parallel efforts to usher in a plethora of regional trade agreements and economic unions.

Given the uncertainty of the multilateral agreement under the ambit of the World Trade Organization, which has been dragging on for years, efforts to form regional agreements are picking up. Although many of them are overlapping, 2015 could see some progress being made on at least some of the deals.

They will have a significant impact on global trade. It is an opportunity for countries that seek to diversify their trade partners to closely follow the deals that are being put in place, to get first-mover advantage.

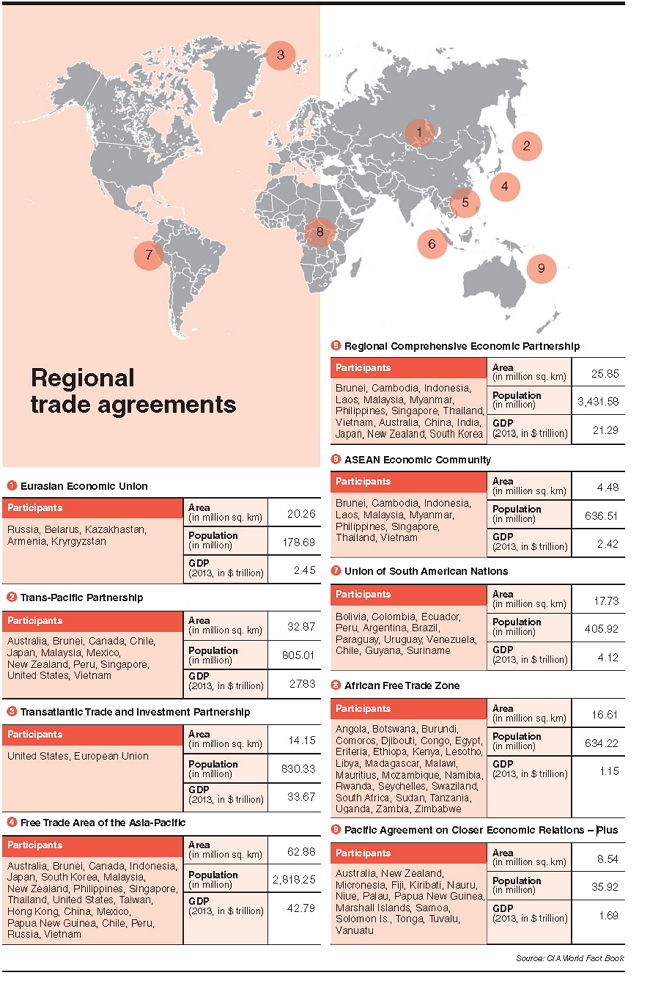

Eurasian Economic Union

First off the block is the Eurasian Economic Union that is still “warm from the oven.” The Commonwealth of Independent States established an economic community in 2001 with the aim of creating a fully fledged common market. However, as it was not making much headway, the leaders of the CIS gathered in Minsk in October 2014 to formally cancel the 14-year-old setup to pave the way for the EEU to be the largest common market in the ex-Soviet Union region.

The treaty on the establishment of the EEU, which just launched on Jan. 1, is the basic document defining the accords between Russia, Belarus and Kazakhstan for the free movement of goods, services, capital and labor and conducting coordinated, agreed or common policies in key economic sectors such as energy, industry, agriculture and transport.

It is sought to rival the European Union and seeks to be the most advanced organization for regional cooperation the former Soviet bloc has seen. Armenia recently joined the union and Kyrgyzstan is expected to join on May 1, with more countries likely to follow.

Although many Western countries are concerned that it is simply a resurrected version of the Soviet Union, the EEU is a powerful economic bloc that accounts for one-fifth of the world’s gas reserves and around 15 percent of its oil. With the start of a new year, a new and serious geopolitical player is indeed emerging, and other emerging markets had better start paying close attention.

Trans-Pacific Partnership

The most talked-about deal in 2014, the Trans-Pacific Partnership, is a proposed regional regulatory and investment treaty that has gained traction recently, but seems to be stuck in a limbo. As of now, 12 countries throughout the Asia-Pacific region have participated in negotiations on the TPP: Australia, Brunei Darussalam, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, the United States and Vietnam. South Korea has expressed interest in joining but has not taken a step forward.

The agreement intends to “enhance trade and investment among the TPP partner countries, to promote innovation, economic growth and development, and to support the creation and retention of jobs.”

If concluded as envisioned, the TPP potentially could eliminate tariff and nontariff barriers to trade and investment among the parties and could serve as a template for a future trade pact among APEC members and potentially other countries.

Over 20 chapters are under discussion in the negotiations. In many cases, the rules being negotiated are intended to be more rigorous than comparable rules found in the WTO.

As the countries that make up the TPP negotiating partners include advanced industrialized, middle income, and developing economies, the TPP, if implemented, may involve restructuring and reform of some participants’ economies. It also has the potential to spur economic growth in the region.

So far 20 formal rounds of TPP negotiations have been held, but the members have not reached a consensus on a number of contentious issues like intellectual property and liberalization of agricultural markets. Another problem has been that, the U.S. could not proceed because of political difficulties at home regarding the passage of a Trade Promotion Authority by Congress.

Transatlantic Trade and Investment Partnership

The so-called “mega deal,” the Transatlantic Trade and Investment Partnership is a trade agreement that is presently being negotiated between the European Union and the United States. Talks started in July 2013, but have faced a lot of opposition from civil society and trade unions in Europe.

The aim is to increase trade and investment between the EU and the U.S. by unleashing the untapped potential of a truly transatlantic marketplace. The agreement is expected to create jobs and growth by delivering better access to the U.S. market, achieving greater regulatory compatibility between the EU and the U.S., and paving the way for setting global standards.

In more concrete terms, the goal will be to eliminate duties and other restrictions for trade in goods. Freeing up commercial services, providing the highest possible protection, certainty and level playing field for European investors in the U.S., and increasing access to U.S. public procurement markets are also objectives.

The T-TIP negotiations will also look at opening both markets for services, investment, and public procurement. They could also shape global rules on trade. The seventh round of negotiations on the agreement concluded on Oct. 3, 2014.

Together, the European Union and the United States account for about half of world GDP and one-third of global trade flows. Latest estimates show that a comprehensive and ambitious agreement between the EU and the U.S. could bring overall annual gains of 0.5 percent increase in GDP for the EU and a 0.4 percent increase in GDP for the U.S. by 2027. While the road is quite long, all eyes are on this deal and some progress may be made in 2015.

Free Trade Area of the Asia-Pacific

A road map for the Free Trade Area of the Asia-Pacific was sketched out at the recent Asia-Pacific Economic Cooperation Summit in Beijing.

Ministers of the 21 APEC member nations agreed to “launch and comprehensively and systemically push forward the FTAAP process.”

In the summit declaration, it was stated that the rules-based multilateral trading system would remain a key tenet of APEC. The FTAAP should be pursued on the basis of supporting and complementing the multilateral trading system.

“The FTAAP should do more than achieve liberalization in its narrow sense; it should be comprehensive, high quality and incorporate and address ‘next generation’ trade and investment issues.”

A collective strategic study on issues related to the realization of the FTAAP by building on and updating existing studies and past work, providing an analysis of potential economic and social benefits and costs, performing a stock take of FTAs in force in the region, has been announced and will be submitted by the end of 2016.

The member countries account for 40 percent of the world’s population, 54 percent of its economic output and 44 percent of trade, making it a very powerful entity and clearly a deal to watch out for.

It will take a while, but given the interest shown by China, it may proceed faster than the TPP.

Regional Comprehensive Economic Partnership

In what could be a game-changer, the Regional Comprehensive Economic Partnership is a 16-party FTA launched by the leaders of the Association of Southeast Asian Nations ― Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam ― and six of its FTA partners: Australia, China, India, Japan, New Zealand and South Korea.

The negotiations for the agreement started in 2013 and are expected to be concluded by year’s end.

The RCEP would lead to greater economic integration, support equitable economic development and strengthen economic cooperation among the countries involved.

The agreement will cover trade in goods, trade in services, investment, economic and technical cooperation, intellectual property, competition, dispute settlement and other issues.

The sixth round of negotiations took place in New Delhi in the first week of December. However, members were unable to agree on a template for negotiations.

The grouping envisages regional economic integration, leading to the creation of the largest regional trading bloc in the world, accounting for nearly 45 percent of the world’s population with a combined gross domestic product of $21.3 trillion. The regional economic pact aims to cover trade in goods and services, investment, economic and technical cooperation, competition and intellectual property.

As of now, it is unlikely that the 2015 deadline will be met, but one can always be ready for surprises.

ASEAN Economic Community

The ASEAN Economic Community seeks to establish ASEAN as a single market and production base, making ASEAN more dynamic and competitive with new mechanisms and measures to strengthen the implementation of its existing economic initiatives; accelerating regional integration in the priority sectors; facilitating movement of businesspersons, skilled labor and talents; and strengthening the institutional mechanisms.

Other areas of cooperation are to be incorporated later. The AEC envisages key characteristics: a single market and production base; a highly competitive economic region; a region of equitable economic development; and a region fully integrated into the global economy.

Although ASEAN has come a long way toward realizing its goal, the challenges that remain suggest that it may miss its end-2015 deadline.

Union of South American Nations

One dark horse is the Union of South American Nations, which is going to be a regional organization integrating two existing customs unions: Mercosur and the Andean Community of Nations, as part of a continuing process of South American integration. It is also modeled on the European Union and was established in Brasilia, on May 23, 2008, and entered into force on March 11, 2011, but full integration is yet to take place.

On Dec. 5, 2014, the 12 members ― Bolivia, Colombia, Ecuador, Peru, Argentina, Brazil, Paraguay, Uruguay, Venezuela, Chile, Guyana and Suriname ― announced new proposals at a summit meeting in Ecuador.

They have taken steps to create South American citizenship and freedom of movement and also opened the organization’s new permanent headquarters in the Ecuadorian capital of Quito.

Part of this proposal is to create a “single passport” and homologate university degrees in order to give South Americans the right to live, work and study in any UNASUR country and to give legal protection to migrants ― similar to freedom of movement rules for citizens of the European Union.

Plans are also afoot for the advancement of financial integration and sovereignty, such as the Bank of the South and Reserve Fund, a currency exchange system to minimize the use of the dollar in intercontinental trade, the creation of a regional body to settle financial disputes, and a common currency “in the medium term.”

African Free Trade Zone

For long an underestimated region, the East African Community, Common Market for Eastern and Central Africa, and Southern African Development Community have already begun negotiations to merge, which is a precursor to a single trade area across the continent.

Africa’s free trade zone is expected to be operational by the end of 2017. They include Angola, Botswana, Burundi, Comoros, Djibouti, Democratic Republic of Congo, Egypt, Eritrea, Ethiopia, Kenya, Lesotho, Libya, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Rwanda, Seychelles, Swaziland, South Africa, Sudan, Tanzania, Uganda, Zambia and Zimbabwe.

In October 2014, they agreed to launch a tripartite FTA as a way of contributing to economic growth of the blocs and the entire continent. The tripartite FTA will encompass 26 member states from the three blocs with a combined population of 625 million people and a gross domestic product of $1.2 trillion and will account for half of the membership of the African Union.

The free trade area is expected to offer huge opportunities for business and investment and will attract foreign direct investment into the tripartite region. The business community is also expected to benefit from an improved and harmonized trade regime in a 26-nation free trade zone and enjoy the reduced cost of doing business.

Pacific Agreement on Closer Economic Relations ― Plus

The Pacific Agreement on Closer Economic Relations, or PACER, is a framework agreement to deepen trade and investment liberalization in the broader Pacific on a step-by-step basis.

Participants in the PACER Plus negotiations are: Australia, Cook Islands, Federated States of Micronesia, Fiji, Kiribati, Nauru, New Zealand, Niue, Pala, Papua New Guinea, Republic of Marshall Islands, Samoa, Solomon Islands, Tonga, Tuvalu and Vanuatu.

PACER Plus negotiations for a regional trade and economic integration agreement were launched in August 2009. A series of meetings on the PACER Plus were held in Fiji in December 2014 to progress the negotiations. It is expected to boost private sector development and create economic growth and employment opportunities, and bring the Pacific Forum economies closer.

There are some bumps, of course, with many Pacific countries wary of the dominant roles played by Australia and New Zealand.

By Ram Garikipati (ram@heraldcorp.com)

While bilateral free trade agreements, as a means to further the market-opening and rule-making agenda, have been globally picking up steam, there have also been parallel efforts to usher in a plethora of regional trade agreements and economic unions.

Given the uncertainty of the multilateral agreement under the ambit of the World Trade Organization, which has been dragging on for years, efforts to form regional agreements are picking up. Although many of them are overlapping, 2015 could see some progress being made on at least some of the deals.

They will have a significant impact on global trade. It is an opportunity for countries that seek to diversify their trade partners to closely follow the deals that are being put in place, to get first-mover advantage.

Eurasian Economic Union

First off the block is the Eurasian Economic Union that is still “warm from the oven.” The Commonwealth of Independent States established an economic community in 2001 with the aim of creating a fully fledged common market. However, as it was not making much headway, the leaders of the CIS gathered in Minsk in October 2014 to formally cancel the 14-year-old setup to pave the way for the EEU to be the largest common market in the ex-Soviet Union region.

The treaty on the establishment of the EEU, which just launched on Jan. 1, is the basic document defining the accords between Russia, Belarus and Kazakhstan for the free movement of goods, services, capital and labor and conducting coordinated, agreed or common policies in key economic sectors such as energy, industry, agriculture and transport.

It is sought to rival the European Union and seeks to be the most advanced organization for regional cooperation the former Soviet bloc has seen. Armenia recently joined the union and Kyrgyzstan is expected to join on May 1, with more countries likely to follow.

Although many Western countries are concerned that it is simply a resurrected version of the Soviet Union, the EEU is a powerful economic bloc that accounts for one-fifth of the world’s gas reserves and around 15 percent of its oil. With the start of a new year, a new and serious geopolitical player is indeed emerging, and other emerging markets had better start paying close attention.

Trans-Pacific Partnership

The most talked-about deal in 2014, the Trans-Pacific Partnership, is a proposed regional regulatory and investment treaty that has gained traction recently, but seems to be stuck in a limbo. As of now, 12 countries throughout the Asia-Pacific region have participated in negotiations on the TPP: Australia, Brunei Darussalam, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, the United States and Vietnam. South Korea has expressed interest in joining but has not taken a step forward.

The agreement intends to “enhance trade and investment among the TPP partner countries, to promote innovation, economic growth and development, and to support the creation and retention of jobs.”

If concluded as envisioned, the TPP potentially could eliminate tariff and nontariff barriers to trade and investment among the parties and could serve as a template for a future trade pact among APEC members and potentially other countries.

Over 20 chapters are under discussion in the negotiations. In many cases, the rules being negotiated are intended to be more rigorous than comparable rules found in the WTO.

As the countries that make up the TPP negotiating partners include advanced industrialized, middle income, and developing economies, the TPP, if implemented, may involve restructuring and reform of some participants’ economies. It also has the potential to spur economic growth in the region.

So far 20 formal rounds of TPP negotiations have been held, but the members have not reached a consensus on a number of contentious issues like intellectual property and liberalization of agricultural markets. Another problem has been that, the U.S. could not proceed because of political difficulties at home regarding the passage of a Trade Promotion Authority by Congress.

Transatlantic Trade and Investment Partnership

The so-called “mega deal,” the Transatlantic Trade and Investment Partnership is a trade agreement that is presently being negotiated between the European Union and the United States. Talks started in July 2013, but have faced a lot of opposition from civil society and trade unions in Europe.

The aim is to increase trade and investment between the EU and the U.S. by unleashing the untapped potential of a truly transatlantic marketplace. The agreement is expected to create jobs and growth by delivering better access to the U.S. market, achieving greater regulatory compatibility between the EU and the U.S., and paving the way for setting global standards.

In more concrete terms, the goal will be to eliminate duties and other restrictions for trade in goods. Freeing up commercial services, providing the highest possible protection, certainty and level playing field for European investors in the U.S., and increasing access to U.S. public procurement markets are also objectives.

The T-TIP negotiations will also look at opening both markets for services, investment, and public procurement. They could also shape global rules on trade. The seventh round of negotiations on the agreement concluded on Oct. 3, 2014.

Together, the European Union and the United States account for about half of world GDP and one-third of global trade flows. Latest estimates show that a comprehensive and ambitious agreement between the EU and the U.S. could bring overall annual gains of 0.5 percent increase in GDP for the EU and a 0.4 percent increase in GDP for the U.S. by 2027. While the road is quite long, all eyes are on this deal and some progress may be made in 2015.

Free Trade Area of the Asia-Pacific

A road map for the Free Trade Area of the Asia-Pacific was sketched out at the recent Asia-Pacific Economic Cooperation Summit in Beijing.

Ministers of the 21 APEC member nations agreed to “launch and comprehensively and systemically push forward the FTAAP process.”

In the summit declaration, it was stated that the rules-based multilateral trading system would remain a key tenet of APEC. The FTAAP should be pursued on the basis of supporting and complementing the multilateral trading system.

“The FTAAP should do more than achieve liberalization in its narrow sense; it should be comprehensive, high quality and incorporate and address ‘next generation’ trade and investment issues.”

A collective strategic study on issues related to the realization of the FTAAP by building on and updating existing studies and past work, providing an analysis of potential economic and social benefits and costs, performing a stock take of FTAs in force in the region, has been announced and will be submitted by the end of 2016.

The member countries account for 40 percent of the world’s population, 54 percent of its economic output and 44 percent of trade, making it a very powerful entity and clearly a deal to watch out for.

It will take a while, but given the interest shown by China, it may proceed faster than the TPP.

Regional Comprehensive Economic Partnership

In what could be a game-changer, the Regional Comprehensive Economic Partnership is a 16-party FTA launched by the leaders of the Association of Southeast Asian Nations ― Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam ― and six of its FTA partners: Australia, China, India, Japan, New Zealand and South Korea.

The negotiations for the agreement started in 2013 and are expected to be concluded by year’s end.

The RCEP would lead to greater economic integration, support equitable economic development and strengthen economic cooperation among the countries involved.

The agreement will cover trade in goods, trade in services, investment, economic and technical cooperation, intellectual property, competition, dispute settlement and other issues.

The sixth round of negotiations took place in New Delhi in the first week of December. However, members were unable to agree on a template for negotiations.

The grouping envisages regional economic integration, leading to the creation of the largest regional trading bloc in the world, accounting for nearly 45 percent of the world’s population with a combined gross domestic product of $21.3 trillion. The regional economic pact aims to cover trade in goods and services, investment, economic and technical cooperation, competition and intellectual property.

As of now, it is unlikely that the 2015 deadline will be met, but one can always be ready for surprises.

ASEAN Economic Community

The ASEAN Economic Community seeks to establish ASEAN as a single market and production base, making ASEAN more dynamic and competitive with new mechanisms and measures to strengthen the implementation of its existing economic initiatives; accelerating regional integration in the priority sectors; facilitating movement of businesspersons, skilled labor and talents; and strengthening the institutional mechanisms.

Other areas of cooperation are to be incorporated later. The AEC envisages key characteristics: a single market and production base; a highly competitive economic region; a region of equitable economic development; and a region fully integrated into the global economy.

Although ASEAN has come a long way toward realizing its goal, the challenges that remain suggest that it may miss its end-2015 deadline.

Union of South American Nations

One dark horse is the Union of South American Nations, which is going to be a regional organization integrating two existing customs unions: Mercosur and the Andean Community of Nations, as part of a continuing process of South American integration. It is also modeled on the European Union and was established in Brasilia, on May 23, 2008, and entered into force on March 11, 2011, but full integration is yet to take place.

On Dec. 5, 2014, the 12 members ― Bolivia, Colombia, Ecuador, Peru, Argentina, Brazil, Paraguay, Uruguay, Venezuela, Chile, Guyana and Suriname ― announced new proposals at a summit meeting in Ecuador.

They have taken steps to create South American citizenship and freedom of movement and also opened the organization’s new permanent headquarters in the Ecuadorian capital of Quito.

Part of this proposal is to create a “single passport” and homologate university degrees in order to give South Americans the right to live, work and study in any UNASUR country and to give legal protection to migrants ― similar to freedom of movement rules for citizens of the European Union.

Plans are also afoot for the advancement of financial integration and sovereignty, such as the Bank of the South and Reserve Fund, a currency exchange system to minimize the use of the dollar in intercontinental trade, the creation of a regional body to settle financial disputes, and a common currency “in the medium term.”

African Free Trade Zone

For long an underestimated region, the East African Community, Common Market for Eastern and Central Africa, and Southern African Development Community have already begun negotiations to merge, which is a precursor to a single trade area across the continent.

Africa’s free trade zone is expected to be operational by the end of 2017. They include Angola, Botswana, Burundi, Comoros, Djibouti, Democratic Republic of Congo, Egypt, Eritrea, Ethiopia, Kenya, Lesotho, Libya, Madagascar, Malawi, Mauritius, Mozambique, Namibia, Rwanda, Seychelles, Swaziland, South Africa, Sudan, Tanzania, Uganda, Zambia and Zimbabwe.

In October 2014, they agreed to launch a tripartite FTA as a way of contributing to economic growth of the blocs and the entire continent. The tripartite FTA will encompass 26 member states from the three blocs with a combined population of 625 million people and a gross domestic product of $1.2 trillion and will account for half of the membership of the African Union.

The free trade area is expected to offer huge opportunities for business and investment and will attract foreign direct investment into the tripartite region. The business community is also expected to benefit from an improved and harmonized trade regime in a 26-nation free trade zone and enjoy the reduced cost of doing business.

Pacific Agreement on Closer Economic Relations ― Plus

The Pacific Agreement on Closer Economic Relations, or PACER, is a framework agreement to deepen trade and investment liberalization in the broader Pacific on a step-by-step basis.

Participants in the PACER Plus negotiations are: Australia, Cook Islands, Federated States of Micronesia, Fiji, Kiribati, Nauru, New Zealand, Niue, Pala, Papua New Guinea, Republic of Marshall Islands, Samoa, Solomon Islands, Tonga, Tuvalu and Vanuatu.

PACER Plus negotiations for a regional trade and economic integration agreement were launched in August 2009. A series of meetings on the PACER Plus were held in Fiji in December 2014 to progress the negotiations. It is expected to boost private sector development and create economic growth and employment opportunities, and bring the Pacific Forum economies closer.

There are some bumps, of course, with many Pacific countries wary of the dominant roles played by Australia and New Zealand.

By Ram Garikipati (ram@heraldcorp.com)

-

Articles by Korea Herald