Most Popular

-

1

Ador CEO denies allegations, accuses Hybe of mistreating NewJeans

-

2

Medical reform committee kicks off despite boycott from doctors

-

3

10-man S. Korea lose to Indonesia to miss out on Paris Olympic football qualification

-

4

Hybe-Ador feud should have limited effect on Hybe's overall performance: analysts

-

5

Second Gimpo civil servant found dead, after apologizing for not finishing work

-

6

DP leader says he will meet Yoon without conditions

-

7

Over 9,000 hotline calls made by stalking victims in 2023

-

8

Monthly users on local streaming platforms outpace Netflix, Disney+

-

9

[Hello India] Hyundai Motor vows to boost 'clean mobility' in India

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

-

10

US will take steps for three-way engagement on nuclear deterrence with S. Korea, Japan: Campbell

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

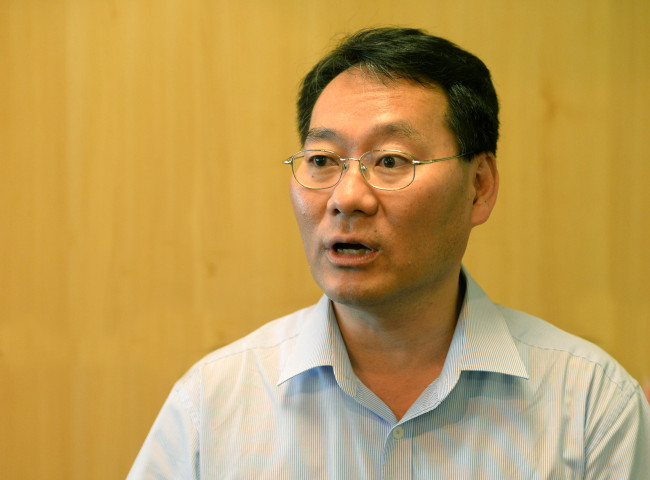

[Herald Interview] Korea faces household debt crisis

By Shin Ji-hyePublished : Sept. 5, 2014 - 20:23

“South Korea’s surging household debt can trigger serious economic crisis,’’ Jun Sung-in, an economics professor at Hongik University told The Korea Herald in an interview Thursday.

“The government’s latest push to ease regulations on home mortgage will increase household debts, which are already getting out of the hand.”

After the Asian financial crisis in 1997, banks turned to household loans, especially in the form of mortgage, as the government tightened rules on corporate lending, in the course of corporate restructuring to pull the country out of the crisis. Before the crisis, Korean banks had heavily depended on interest income from corporate loans.

While household debts have gradually increased over the past decade, it no longer appears safe. According to the OECD, South Korea’s household debt increased by an annual average of 8.7 percent from 2008 to 2013, while the United States and Japan saw a 0.7 percent and 1.1 percent drop respectively. The nation’s household debt exceeded 1,000 trillion won ($977 billion) for the first time last year.

“The government’s push to encourage more debt to buy houses is risky in this aging society where the housing price will eventually fall down. When the housing bubble bursts, the insolvency of the mortgage will bring down the value of other assets,” Jun said.

He said that instead of encouraging more household to take loans, the government should focus on revitalizing the domestic market.

“The government should encourage consumers to spend more money in the domestic market by supporting low-income families or small and medium enterprises through wage increases.”

He pointed out that the consumers who spend money in the domestic markets are usually the low-income people or the middle class, and not the rich.

“People in the lower brackets of income tend to spend their money on food or clothing when they have disposable income. The rich rather invest it in the financial market or buying imported goods, which is not helpful to boosting the domestic market,” he said.

Supporting small and medium enterprises to help raise wages is also important, he said. In order to prevent large companies from suffocating their subcontractors by slashing prices, regulatory intervention is necessary, he said.

“The government can provide financial incentives to large companies that pay more than the market price to their subcontractors. The companies which pay lower prices should pay more taxes,” the professor said.

By Shin Ji-hye (shinjh@heraldcorp.com)