Most Popular

-

1

Ador CEO denies allegations, accuses Hybe of mistreating NewJeans

-

2

Medical reform committee kicks off despite boycott from doctors

-

3

10-man S. Korea lose to Indonesia to miss out on Paris Olympic football qualification

-

4

Hybe-Ador feud should have limited effect on Hybe's overall performance: analysts

-

5

DP leader says he will meet Yoon without conditions

-

6

Second Gimpo civil servant found dead, after apologizing for not finishing work

-

7

Over 9,000 hotline calls made by stalking victims in 2023

-

8

[Hello India] Hyundai Motor vows to boost 'clean mobility' in India

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

-

9

Monthly users on local streaming platforms outpace Netflix, Disney+

-

10

US will take steps for three-way engagement on nuclear deterrence with S. Korea, Japan: Campbell

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

[Carmen M. Reinhart and Kenneth S. Rogoff] Too much debt means the economy can’t grow

By 류근하Published : July 20, 2011 - 18:47

As public debt in advanced countries reaches levels not seen since the end of World War II, there is considerable debate about the urgency of taming deficits with the aim of stabilizing and ultimately reducing debt as a percentage of gross domestic product.

Our empirical research on the history of financial crises and the relationship between growth and public liabilities supports the view that current debt trajectories are a risk to long-term growth and stability, with many advanced economies already reaching or exceeding the important marker of 90 percent of GDP. Nevertheless, many prominent public intellectuals continue to argue that debt phobia is wildly overblown. Countries such as the U.S., Japan and the U.K. aren’t like Greece, nor does the market treat them as such.

Indeed, there is a growing perception that today’s low interest rates for the debt of advanced economies offer a compelling reason to begin another round of massive fiscal stimulus. If Asian nations are spinning off huge excess savings partly as a byproduct of measures that effectively force low-income savers to put their money in bank accounts with low government-imposed interest-rate ceilings ― why not take advantage of the cheap money?

Although we agree that governments must exercise caution in gradually reducing crisis-response spending, we think it would be folly to take comfort in today’s low borrowing costs, much less to interpret them as an “all clear” signal for a further explosion of debt.

Several studies of financial crises show that interest rates seldom indicate problems long in advance. In fact, we should probably be particularly concerned today because a growing share of advanced country debt is held by official creditors whose current willingness to forego short-term returns doesn’t guarantee there will be a captive audience for debt in perpetuity.

Those who would point to low servicing costs should remember that market interest rates can change like the weather. Debt levels, by contrast, can’t be brought down quickly. Even though politicians everywhere like to argue that their country will expand its way out of debt, our historical research suggests that growth alone is rarely enough to achieve that with the debt levels we are experiencing today.

While we expect to see more than one member of the Organization for Economic Cooperation and Development default or restructure their debt before the European crisis is resolved, that isn’t the greatest threat to most advanced economies. The biggest risk is that debt will accumulate until the overhang weighs on growth.

At what point does indebtedness become a problem? In our study “Growth in a Time of Debt,” we found relatively little association between public liabilities and growth for debt levels of less than 90 percent of GDP. But burdens above 90 percent are associated with 1 percent lower median growth. Our results are based on a data set of public debt covering 44 countries for up to 200 years. The annual data set incorporates more than 3,700 observations spanning a wide range of political and historical circumstances, legal structures and monetary regimes.

We aren’t suggesting there is a bright red line at 90 percent; our results don’t imply that 89 percent is a safe debt level, or that 91 percent is necessarily catastrophic. Anyone familiar with doing empirical research understands that vulnerability to crises and anemic growth seldom depends on a single factor such as public debt. However, our study of crises shows that public obligations are often hidden and significantly larger than official figures suggest.

In addition, off-balance sheet guarantees and other creative accounting devices make it even harder to assess the true nature of a country’s debt until a crisis forces everything out into the open. (Just think of the giant U.S. mortgage lenders Fannie Mae and Freddie Mac, whose debt was never officially guaranteed before the 2008 meltdown.)

There also is the question of how broad a measure of public debt to use. Our empirical work concentrates on central-government obligations because state and local data are so limited across time and countries, and government guarantees, as noted, are difficult to quantify over time. (Until we developed our data set, no long-dated cross-country information on central government debt existed.) But state and local debt are important because they so frequently trigger federal government bailouts in a crisis. Official figures for state debts don’t include chronic late payments (arrears), which are substantial in Illinois and California, for example.

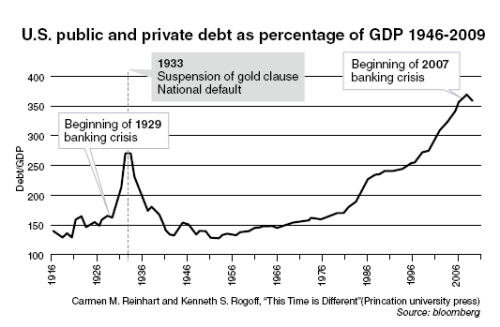

Indeed, it isn’t unusual for governments to absorb large chunks of troubled private debt in a crisis. Taking this into account, chart 1, attached, shows the extraordinarily high level of overall U.S. debts, public and private.

In addition to ex-ante or ex-post government guarantees and other forms of “hidden debts,” any discussion of public liabilities should take into account the demographic challenges across the industrialized world. Our 90 percent threshold is largely based on earlier periods when old-age pensions and health-care costs hadn’t grown to anything near the size they are today. Surely this makes the burden of debt greater.

There is a growing sense that inflation is the endgame to debt buildups. For emerging markets that has often been the case, but for advanced economies, the historical correlation is weaker. Part of the reason for this apparent paradox may be that, especially after World War II, many governments enacted policies that amounted to heavy financial repression, including interest rate ceilings and non-market debt placement. Low statutory interest rates allowed governments to reduce real debt burdens through moderate inflation over a sustained period. Of course, this time could be different, and we shouldn’t entirely dismiss the possibility of elevated inflation as the antidote to debt.

Those who remain unconvinced that rising debt levels pose a risk to growth should ask themselves why, historically, levels of debt of more than 90 percent of GDP are relatively rare and those exceeding 120 percent are extremely rare (see attached chart 2 for U.S. public debt since 1790). Is it because generations of politicians failed to realize that they could have kept spending without risk? Or, more likely, is it because at some point, even advanced economies hit a ceiling where the pressure of rising borrowing costs forces policy makers to increase tax rates and cut government spending, sometimes precipitously, and sometimes in conjunction with inflation and financial repression (which is also a tax)?

Even absent high interest rates, as Japan highlights, debt overhangs are a hindrance to growth.

The relationship between growth, inflation and debt, no doubt, merits further study; it is a question that cannot be settled with mere rhetoric, no matter how superficially convincing.

In the meantime, historical experience and early examination of new data suggest the need to be cautious about surrendering to “this-time-is-different” syndrome and decreeing that surging government debt isn’t as significant a problem in the present as it was in the past.

By Carmen M. Reinhart and Kenneth S. Rogoff

Carmen M. Reinhart is a senior fellow at the Peterson Institute for International Economics in Washington. Kenneth S. Rogoff is a professor of economics at Harvard University. They are co-authors of “This Time is Different: Eight Centuries of Financial Folly.” The opinions expressed are their own. ― Ed.

(Bloomberg)