Most Popular

-

1

Exports to US reach all-time high, widen gap with China

-

2

Trump rekindles criticism: US forces defending 'wealthy' S. Korea 'free of charge'

-

3

[Music in drama] Rekindle a love that slipped through your fingers

![[Music in drama] Rekindle a love that slipped through your fingers](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050484_0.jpg&u=20240501151646)

-

4

S. Korea discussed possible participation in AUKUS Pillar 2 with Australia: defense minister

-

5

[New faces of Assembly] Architect behind ‘audacious initiative’ believes in denuclearized North Korea

![[New faces of Assembly] Architect behind ‘audacious initiative’ believes in denuclearized North Korea](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050627_0.jpg&u=20240502093000)

![[Music in drama] Rekindle a love that slipped through your fingers](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050484_0.jpg&u=20240501151646)

![[New faces of Assembly] Architect behind ‘audacious initiative’ believes in denuclearized North Korea](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050627_0.jpg&u=20240502093000)

-

6

Opposition-led Assembly unilaterally passes bill to probe Marine's death

-

7

Seoul Metro to seek legal action against malicious complaints

-

8

Illit, mired in controversy, remains on Billboard charts for 5th week

-

9

On May Day, labor unions blast Yoon's foreign nanny proposal

-

10

[KH Explains] Will alternative trading platform shake up Korean stock market?

![[KH Explains] Will alternative trading platform shake up Korean stock market?](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050557_0.jpg&u=20240501161906)

![[KH Explains] Will alternative trading platform shake up Korean stock market?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050557_0.jpg&u=20240501161906)

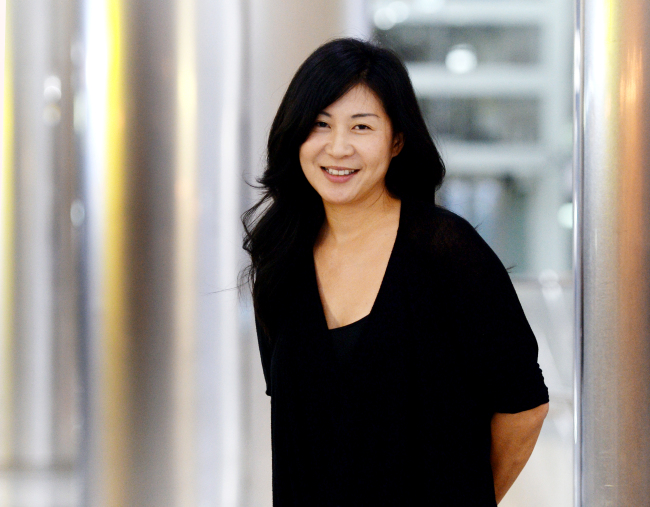

[Herald Interview] Education key to dealing with bitcoin craze

Co-founder of cryptocurrency-turned-venture capitalist urges Korea to study blockchain to remain tech leader

By Son Ji-hyoungPublished : Dec. 15, 2017 - 16:53

But the bitcoin craze does not necessarily mean investors understand the way blockchain works, or that they can even tell the difference between cryptocurrency and blockchain, since they are more interested in high returns than the underlying technology.

Cryptocurrencies are digital currencies encrypted and traded on blockchain-powered networks. A blockchain itself is a distributed computing system with much broader uses than just cryptocurrencies, from financial security to logistics, agriculture and voting.

The two are mixed up, even by financial experts, illustrated recently in a local column in which the author said that when he told some financiers that he was interested in blockchain technology, they candidly asked how much profit he made.

To keep Korea as a true leader in technology amid a huge, international technological shift, turning a blind eye to blockchain is not an option for the government, according to Joyce Kim, co-founder of SparkChain Capital, a venture capital firm dedicated to investing in blockchain startups, and co-founder of Stellar, the 15th-largest cryptocurrency by market cap.

One way to fight the excessive bitcoin craze, mainly fueled by speculation, could be the government’s effort to become a world blockchain education leader, ultimately for the sake of financial consumers’ protection, she suggested.

“Making people smarter is better than making people afraid,” Kim said. “(The government) should be doing a lot of education, not just saying, ‘Be careful.’”

Kim, 39, was the first woman and first ethnic Korean in the US to have created a cryptocurrency coin surpassing $2 billion in total value.

Over 8.1 billion tokens, now called Lumens, have been issued on the Stellar protocol by nonprofit Stellar Development Foundation since 2014, when it forked off from the fourth-largest cryptocurrency Ripple. The upgraded protocol by Stellar can be used for cross-border payments, microfinance, currency exchange and remittance, core functions that complete technology for low-cost banking, especially in countries that lack conventional banking infrastructure.

To lead it or fight it

To Kim, regulations on cryptocurrency businesses, like those announced Wednesday by a pangovernmental task force, appear inevitable to bring bitcoin prices under control.

But the government will not, and cannot, “stop the technology from happening.”

“Because the technology is so resilient, (bitcoin) doesn’t go away.” Kim said. “It just hides better.”

Having the cryptocurrency business out in the light instead of banning it not only helps the government take control of it, but also bolsters people’s awareness and need for education.

“If (a cryptocurrency ecosystem) gets open, you can learn and have discussions with people and so do the appropriate financial oversight of this,” Kim said. “But when it’s hidden, it’s like everything else is in the dark so you can’t see it.”

“There will always be some people who understand the blockchain, but there will always be people who don’t,” she said. “As a technology community, we try to communicate with as many people as we can.”

Although dwarfed by the bitcoin craze, blockchain technologies in noncryptocurrency businesses have also been developing in Korea, Kim said.

She gave the example of Blocko, a startup that teamed up with Gyeonggi Province to establish a blockchain-powered online voting system this year by making use of its original smart contract technology.

Moreover, Sogang University is poised to open the first college of blockchain software in Korea in its graduate school starting next year.

“As a Korean, I want to do everything I can to help Korean companies do well with blockchain abroad and in here, because we’ve become the leader very fast,” Kim said.

Nevertheless, such efforts have largely stayed out of the public eye. Instead, Koreans have largely regarded the blockchain community as a hotbed of crime, including cryptocurrency-linked scams.

Kim said that knowing how to find out the “DNA of the community,” based on her experience in the blockchain business for two years as a Stellar co-founder, will help her set a standard for investment.

“Blockchain is at a critical point, because it can be used to build very great things that can transform society, or can be used to build very selfish things,” she said.

Making connections in new worlds

Before jumping into the cryptocurrency business, Kim was an attorney, a counselor for startups, the head of K-pop news outlet Soompi and co-founder of an e-commerce app.

Another Stellar co-founder, Jed McCaleb, was the creator of the peer-to-peer file-sharing eDonkey Network, now-defunct cryptocurrency exchange Mt. Gox and cryptocurrency Ripple.

“In technology, you progress quickly to new ideas,” Kim said, referring to changes in her career path. “The idea that experience can only be gained in one field is an old economy view.”

The two got to know one another in 2011 from a shared interest in surfing. McCaleb had just left Mt. Gox and was about to found Ripple.

Three years later, the two came together to establish the Stellar Development Foundation with the first 1 million tokens. The code, which originated from the Ripple protocol, had to be rewritten for a year to support the interbank transactions of Lumens.

Money would be remitted, within seconds at the fastest, among licensed financial providers around the world that integrated with Stellar protocol. Physical financial infrastructure would not be required to connect nations and their currencies, so that governments would be able to cut costs.

Also as a part of a move to enhance accessibility, the nonprofit foundation has distributed giveaway Lumens, she added.

Kim’s challenge as an ethnic Korean living abroad spawned the idea of a financial system without borders, recalling when she had to remit money from the United States to her grandmother in Korea.

“I used my experience as a Korean-American, a Korean who lived abroad, and the problems I had with this, to figure out how to build Stellar,” Kim said.

Stellar gained attention after sealing a deal with IBM in October. A month later, its market cap crossed the $1 billion mark, then within a couple of weeks approached $3 billion.

Holding dual identities, her journey to connect for the good of society will continue, Kim said.

“I live in the crypto world and I live in the world of social good, and I live in Korean world and I live in American world,” she said. “So I want to be able to make those connections.”

By Son Ji-hyoung

(consnow@heraldcorp.com)

![[Today’s K-pop] Stray Kids go gold in US with ‘Maniac’](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=642&simg=/content/image/2024/05/02/20240502050771_0.jpg&u=)