Most Popular

-

1

Medical profs at top hospitals suspend surgeries, clinics

-

2

Exports to US reach all-time high, widen gap with China

-

3

Trump rekindles criticism: US forces defending 'wealthy' S. Korea 'free of charge'

-

4

Samsung chip business back on track, logs W1.9tr operating profit in Q1

-

5

Shinsegae faces showdown with investors over SSG.com's delayed IPO

-

6

Hopes rise for possible Gaza truce deal

-

7

Ex-pro baseball player who killed debtor appeals sentence

-

8

S. Korea discussed possible participation in AUKUS Pillar 2 with Australia: defense minister

-

9

[New faces of Assembly] Architect behind ‘audacious initiative’ believes in denuclearized North Korea

![[New faces of Assembly] Architect behind ‘audacious initiative’ believes in denuclearized North Korea](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050627_0.jpg&u=20240502093000)

-

10

[Music in drama] Rekindle a love that slipped through your fingers

![[Music in drama] Rekindle a love that slipped through your fingers](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050484_0.jpg&u=20240501151646)

![[New faces of Assembly] Architect behind ‘audacious initiative’ believes in denuclearized North Korea](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050627_0.jpg&u=20240502093000)

![[Music in drama] Rekindle a love that slipped through your fingers](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/01/20240501050484_0.jpg&u=20240501151646)

[ANALYST REPORT] Credit rating upgrade to serve as mid- to long-term positive

By 박한나Published : Aug. 10, 2016 - 15:39

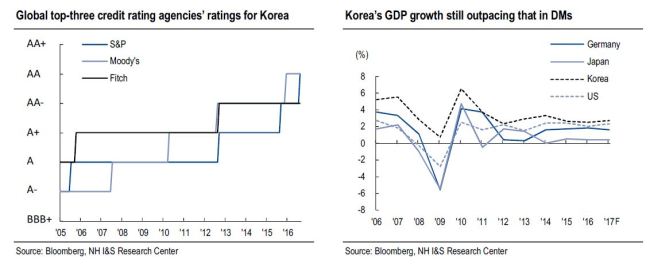

On Aug 8, Standard & Poor’s (S&P) upgraded Korea’s sovereign credit rating by one notch from AA- to AA.

We believe that this credit rating upgrade will positively impact the domestic bond market over the mid- to long run as it should help sustain foreign capital inflows and make it easier for Korea to adjust its monetary policy. Over the near term, however, due to the price burden, the bond market should remain range bound before gradually regaining strength.

▶Overview of credit rating upgrade

S&P has raised its credit rating for Korea to AA (from AA-; maintained its outlook as ‘stable’), citing—as main grounds for the higher rating—Korea’s steady economic growth, sound fiscal position, ability to flexibly adjust fiscal and monetary policies, and stable trading environment.

▶Implications of credit rating upgrade

In our view, S&P’s upgrade is significant, particularly for the following reasons:

First, the status of won-denominated bonds as safe assets should solidify. Having suffered from foreign capital outflows during the 1997 Asian Financial Crisis and the 2008 global financial crisis, Korea has been subjected to continued controversy as to whether won-denominated bonds are safe assets. Yet, given that foreigners’ won-denominated bond holdings have been steadily rising since 2010 (despite the presence of negative events), it seems that won-denominated bonds have been increasingly seen as safe assets. Against this backdrop, we expect this credit rating upgrade to solidify the status of won-denominated assets as safe assets.

Second, Korea will likely secure greater room to adjust its monetary policy. While Switzerland, Sweden, and Denmark are small open economies and do not have key currencies, they have all adopted negative interest rates thanks in part to their stable currencies (helped by their AAA sovereign credit rating). Given that Korea now boasts a AA rating (two notches below the highest rating (AAA)) from two major credit ratings agencies (S&P and Moody’s), any additional base rate cut should only have a limited effect on the won. This suggests that the Bank of Korea (BOK) will enjoy greater discretion to adjust the base rate.

▶Implications of credit rating upgrade

The credit rating upgrade bodes well for the bond market over the mid- to long term—it should help sustain foreign capital inflows and give the BOK more room to adjust its monetary policy.

However, the bond valuation burden (due to the prolonged yield falls and negative yield spread between the 10yr KTB and 10yr US TB) is a cause for concern over the short term.

Also, as the BOK is expected to cut the base rate again in October, we believe that monetary policy momentum will remain lackluster for the time being. Consequently, we expect the bond market to remain range bound before gradually turning bullish. We advise expanding duration upon yield hikes.

Source: NH Investment & Securities

We believe that this credit rating upgrade will positively impact the domestic bond market over the mid- to long run as it should help sustain foreign capital inflows and make it easier for Korea to adjust its monetary policy. Over the near term, however, due to the price burden, the bond market should remain range bound before gradually regaining strength.

▶Overview of credit rating upgrade

S&P has raised its credit rating for Korea to AA (from AA-; maintained its outlook as ‘stable’), citing—as main grounds for the higher rating—Korea’s steady economic growth, sound fiscal position, ability to flexibly adjust fiscal and monetary policies, and stable trading environment.

▶Implications of credit rating upgrade

In our view, S&P’s upgrade is significant, particularly for the following reasons:

First, the status of won-denominated bonds as safe assets should solidify. Having suffered from foreign capital outflows during the 1997 Asian Financial Crisis and the 2008 global financial crisis, Korea has been subjected to continued controversy as to whether won-denominated bonds are safe assets. Yet, given that foreigners’ won-denominated bond holdings have been steadily rising since 2010 (despite the presence of negative events), it seems that won-denominated bonds have been increasingly seen as safe assets. Against this backdrop, we expect this credit rating upgrade to solidify the status of won-denominated assets as safe assets.

Second, Korea will likely secure greater room to adjust its monetary policy. While Switzerland, Sweden, and Denmark are small open economies and do not have key currencies, they have all adopted negative interest rates thanks in part to their stable currencies (helped by their AAA sovereign credit rating). Given that Korea now boasts a AA rating (two notches below the highest rating (AAA)) from two major credit ratings agencies (S&P and Moody’s), any additional base rate cut should only have a limited effect on the won. This suggests that the Bank of Korea (BOK) will enjoy greater discretion to adjust the base rate.

▶Implications of credit rating upgrade

The credit rating upgrade bodes well for the bond market over the mid- to long term—it should help sustain foreign capital inflows and give the BOK more room to adjust its monetary policy.

However, the bond valuation burden (due to the prolonged yield falls and negative yield spread between the 10yr KTB and 10yr US TB) is a cause for concern over the short term.

Also, as the BOK is expected to cut the base rate again in October, we believe that monetary policy momentum will remain lackluster for the time being. Consequently, we expect the bond market to remain range bound before gradually turning bullish. We advise expanding duration upon yield hikes.

Source: NH Investment & Securities