Most Popular

-

1

Korean labor force to shrink by 10 million by 2044: report

-

2

[AtoZ Korean Mind] Does your job define who you are? Should it?

![[AtoZ Korean Mind] Does your job define who you are? Should it?](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/06/20240506050099_0.jpg&u=)

-

3

Allegations surrounding BTS resurface, enraged fans demand apology

-

4

Students with history of violence will be barred from becoming teachers

-

5

Top prosecutor pledges 'speedy, strict' probe into first lady's luxury bag allegations

![[AtoZ Korean Mind] Does your job define who you are? Should it?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/05/06/20240506050099_0.jpg&u=)

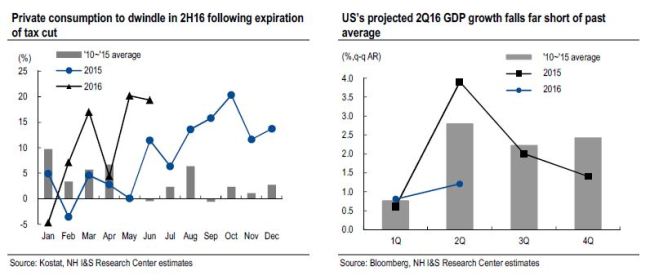

Despite price burdens, the bond market should continue to strengthen on economic uncertainties and favorable demand-supply conditions. As such, we suggest waiting for the next base rate cut (expected in September or October) and expanding duration on KTBs upon yield rises.

Global bond market outlook

Developed markets: The yield uptrend in the US bond market (on lessening Brexit-related concerns) came to an end last week. This week, the US bond market is set to strengthen—on the recent drop in oil price and greater monetary easing activity in major economies—with the 10yr US TB yield expected to range 1.30~1.55%. Meanwhile, the US TB-Bund spread and US 2/10yr spread are both projected to narrow, and the EMU spread will likely remain range bound.

Asia (excluding Japan): Given both the global trend towards monetary easing and ongoing ample capital inflows into EM bond funds, we expect Asian bond markets to continue to gather force. The Indonesian bond market in particular should gain momentum as a new tax amnesty bill has recently come into effect (Jul 18).

Domestic bond market outlook

After strengthening in early July, the domestic bond market has been range bound since the middle of the month. Price burdens are growing heavier—yields on 5yr KTBs are lower than the base rate, the 3/10yr spread has narrowed to below 20bps, and yields on 10yr KTBs are around 10bps lower than those for 10yr US TBs.

However, we believe that the domestic bond market will continue strengthening as: 1) Brexit-related economic uncertainties remain in play (though have dissipated somewhat); 2) the recent oil price fall has reignited deflation fears; 3) worries towards the domestic economy are rising due to the end of a special consumption tax cut, a possible delay in the execution of a supplementary budget, and the approaching (September) implementation of new anti-corruption legislation; and 4) demand-supply conditions for the bond market should remain favorable.

We point out that the KTB issuance amount in 2H16 will shrink h-h. Meanwhile, given that the swap point has been lowered, we forecast that domestic investors will decrease their foreign investments and expand their domestic investments.

Moreover, responding to the upcoming introduction of IFRS 4 Phase II accounting standards (requires insurance companies to beef up their capital bases), insurance players will likely increase their bond investment activity.

Against this backdrop, we expect the bond market to strengthen slightly, with the 3yr KTB yield likely ranging between 1.13~1.25%, the 5yr KTB yield between 1.14~1.28%, and the 10yr KTB yield between 1.27~1.44%.

Despite the price burdens, the bond market should continue strengthening on economic uncertainties and favorable demand-supply conditions. As such, we suggest waiting for the next base rate cut (expected in September or October) and expanding duration on KTBs upon yield rises.

Trading recommendations

We advise: 1) remaining long on 10yr KTBis; 2) remaining long on 10yr KTBs; 3) remaining long on 5yr Indonesian bonds; 4) maintaining a US 2/10yr flattener position; and 5) remaining long on 5yr Thai bonds.

Source: NH Investment & Securities

Global bond market outlook

Developed markets: The yield uptrend in the US bond market (on lessening Brexit-related concerns) came to an end last week. This week, the US bond market is set to strengthen—on the recent drop in oil price and greater monetary easing activity in major economies—with the 10yr US TB yield expected to range 1.30~1.55%. Meanwhile, the US TB-Bund spread and US 2/10yr spread are both projected to narrow, and the EMU spread will likely remain range bound.

Asia (excluding Japan): Given both the global trend towards monetary easing and ongoing ample capital inflows into EM bond funds, we expect Asian bond markets to continue to gather force. The Indonesian bond market in particular should gain momentum as a new tax amnesty bill has recently come into effect (Jul 18).

Domestic bond market outlook

After strengthening in early July, the domestic bond market has been range bound since the middle of the month. Price burdens are growing heavier—yields on 5yr KTBs are lower than the base rate, the 3/10yr spread has narrowed to below 20bps, and yields on 10yr KTBs are around 10bps lower than those for 10yr US TBs.

However, we believe that the domestic bond market will continue strengthening as: 1) Brexit-related economic uncertainties remain in play (though have dissipated somewhat); 2) the recent oil price fall has reignited deflation fears; 3) worries towards the domestic economy are rising due to the end of a special consumption tax cut, a possible delay in the execution of a supplementary budget, and the approaching (September) implementation of new anti-corruption legislation; and 4) demand-supply conditions for the bond market should remain favorable.

We point out that the KTB issuance amount in 2H16 will shrink h-h. Meanwhile, given that the swap point has been lowered, we forecast that domestic investors will decrease their foreign investments and expand their domestic investments.

Moreover, responding to the upcoming introduction of IFRS 4 Phase II accounting standards (requires insurance companies to beef up their capital bases), insurance players will likely increase their bond investment activity.

Against this backdrop, we expect the bond market to strengthen slightly, with the 3yr KTB yield likely ranging between 1.13~1.25%, the 5yr KTB yield between 1.14~1.28%, and the 10yr KTB yield between 1.27~1.44%.

Despite the price burdens, the bond market should continue strengthening on economic uncertainties and favorable demand-supply conditions. As such, we suggest waiting for the next base rate cut (expected in September or October) and expanding duration on KTBs upon yield rises.

Trading recommendations

We advise: 1) remaining long on 10yr KTBis; 2) remaining long on 10yr KTBs; 3) remaining long on 5yr Indonesian bonds; 4) maintaining a US 2/10yr flattener position; and 5) remaining long on 5yr Thai bonds.

Source: NH Investment & Securities

![[K-pop's dilemma] Is Hybe-Ador conflict a case of growing pains?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=642&simg=/content/image/2024/05/07/20240507050746_0.jpg&u=)