Most Popular

-

1

Ador CEO denies allegations, accuses Hybe of mistreating NewJeans

-

2

Medical reform committee kicks off despite boycott from doctors

-

3

10-man S. Korea lose to Indonesia to miss out on Paris Olympic football qualification

-

4

DP leader says he will meet Yoon without conditions

-

5

Over 9,000 hotline calls made by stalking victims in 2023

-

6

[Hello India] Hyundai Motor vows to boost 'clean mobility' in India

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

-

7

Monthly users on local streaming platforms outpace Netflix, Disney+

-

8

US will take steps for three-way engagement on nuclear deterrence with S. Korea, Japan: Campbell

-

9

Second Gimpo civil servant found dead, after apologizing for not finishing work

-

10

Seoul to promote luxurious side of the city

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

Markets brace for rate rises

Floating rate funds emerge as alternatives to bonds, equities

By Park Hyung-kiPublished : May 15, 2014 - 20:44

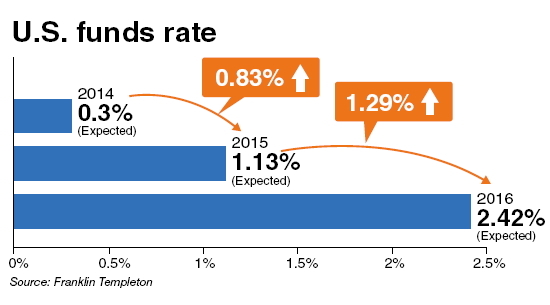

The U.S. federal funds rate is poised to increase as the world’s largest economy recovers and sees its unemployment rate decline and inflation rise to target levels.

The global market had pondered about when the Federal Reserve would actually make its move until Fed Chair Janet Yellen shed some light on the future direction of its monetary policy.

The global market had pondered about when the Federal Reserve would actually make its move until Fed Chair Janet Yellen shed some light on the future direction of its monetary policy.

She said in March that the central bank could raise the interest rate about “six months” after it ends the bond-purchasing program, which the Fed has been scaling back since early this year.

With the era of near-zero rates expected to last probably until early 2015, that could also affect other central banks, including the Bank of Korea, and global investors and asset managers would need to realign their portfolios in response to the rising rates.

Investment instruments such as floating rate funds have emerged in Korea that could help investors hedge against increasing interest rates as their yields follow the benchmark short-term rates.

Floating rate funds, for instance, offered for the first time in Korea by Franklin Templeton Investments, directly invest in U.S. bank loans made to companies with credit ratings of below S&P’s “BBB minus.”

The coupon rates of the funds adjust to the benchmark short-term reference rates such as the U.S. federal funds rate and the London Interbank Offered Rate. When such benchmarks increase, fund investors will be able to gain returns, instead of seeing the values of their traditional bonds drop as rates increase.

They may look like high-yield junk bonds issued by companies with below-investment-grade ratings.

But Franklin Templeton, which has been managing floating rate funds over the last 16 years with assets worth some 17 trillion won ($16.6 billion), said that the funds are invested in senior secured loans backed by collateral.

The funds tend to have lower risks than junk bonds as bank loans are extended to companies in exchange for tangible and intangible assets such as real estate holdings and intellectual properties, the asset manager said.

The default rate of U.S. bank loans has reached a record low of around 2 percent on the back of an economic recovery as of the end of April 2013, according to Moody’s and Shinhan Investment.

“The funds allow (investors) to reduce exposure to risks stemming from rate rises, and provide stable returns,” said Jeon Yong-bae, president and CEO of Franklin Templeton Investment Trust Management Korea.

“They can be reasonable investment products on expectations of rate rises.”

In a case study presented by Franklin Templeton, bank loan funds were able to generate returns of 5.69 percent in 2005, when the U.S. Fed increased its federal funds rate to 2 percent, compared to returns of 3 percent for 10-year Treasury notes and 2.26 percent for high-yield bonds.

However, as Franklin Templeton Korea said, they could be seen as reasonable yet “alternative” investment instruments to other types of funds that invest in traditional bonds, equities and other assets.

Like any other investment assets, whether the market faces rising or falling rates, floating rate funds entail potential risks that could generate losses for investors, as they carry “relatively high credit risks.”

“Also, Korean investors can face losses on foreign exchange volatility,” the asset manager said.

Given that the market has always moved unpredictably despite signs of an economic recovery, it would be best, especially for retail investors, to analyze the market and receive advice from asset managers with long-standing experience in the field before planning and making investments.

By Park Hyong-ki (hkp@heraldcorp.com)