Most Popular

-

1

Ador CEO denies allegations, accuses Hybe of mistreating NewJeans

-

2

Medical reform committee kicks off despite boycott from doctors

-

3

10-man S. Korea lose to Indonesia to miss out on Paris Olympic football qualification

-

4

DP leader says he will meet Yoon without conditions

-

5

Over 9,000 hotline calls made by stalking victims in 2023

-

6

[Hello India] Hyundai Motor vows to boost 'clean mobility' in India

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

-

7

US will take steps for three-way engagement on nuclear deterrence with S. Korea, Japan: Campbell

-

8

Monthly users on local streaming platforms outpace Netflix, Disney+

-

9

NewJeans fans send protest truck against agency chief in conflict with Hybe

-

10

Seoul to promote luxurious side of the city

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

Three issues concerning the world’s carbon markets and their prospects

By Korea HeraldPublished : Dec. 24, 2013 - 19:57

The Kyoto Protocol adopted at the Framework Convention on Climate Change in 1997 went into effect in 2005. The protocol required advanced nations to reduce their greenhouse gas emissions by an average of 5.2 percent below 1990 levels between 2008 and 2012. To meet the targets, 25 EU states created the Emissions Trading System in 2005, allowing 1,963 companies to trade part of their emissions quota.

Along with the ETS, the EU opened the world’s first carbon market, and Asia-Pacific and North America followed suit. Currently, 10 carbon markets are operating worldwide. The EU, Switzerland, New Zealand, Kazakhstan and Australia operate carbon markets on a national level, and the U.S., Japan and China on a regional level. The EU’s carbon market is the world’s biggest, accounting for 73 percent of the trading.

Total trading volume in the global carbon market was 10.9 billion tons of carbon dioxide (tCO2) in 2012, up 25.3 percent from 2011. But the trading amount declined 36.7 percent to 6.2 billion euros during the same period because of a 49.5 percent decline in the cost of carbon permits. Worsening economic conditions in the EU led to a dramatic drop in carbon emissions, leading to a sharp rise in the market supply of emission rights.

Will the EU carbon market recover from fall?

The battering that the U.S. and EU economies have suffered since the 2008 global financial crisis has naturally led to lower carbon emissions and a large surplus of carbon emissions rights. The oversupply has worsened since 2009. By the end of 2012, approximately 2 billion excess tCO2 of surplus emissions rights were available on the market. Prices for the rights in the EU declined from 14 euros per tCO2 in January 2011 to 4.6 euros per tCO2 in August 2013, only a third of their former price.

The EU plans to address the contraction in the carbon market through three initiatives: Reducing the supply of emissions permits, increasing demand for the permits, and balancing supply and demand. To reduce the supply, the EU is shifting from capping individual countries to an EU-wide limit, strengthening assessments of cap amounts, reducing caps by year, and limiting emission rights trading. To increase demand for the emissions rights, air transport will be made eligible for carbon trading.

Through this, about 200 million tCO2 of the total allotment, or about 10 percent, will be increased. Finally, by delaying the time of release of some rights, the EU can resolve the oversupply in the short term.

Will China’s cap and trade succeed?

China, the world’s largest carbon emitter, has not been able to reduce emissions despite a massive clean development mechanism project. After emitting 7 billion tCO2 of greenhouse gas in 2007, China emitted 9.7 billion tCO2 in 2011, for a four-year average annual rise of 8.5 percent. In contrast, the U.S. and EU’s annual emissions declined 2.1 percent and 2.2 percent on average, respectively. China has promoted more than 3,000 CDM projects investing more than $200 billion, but faces limits in reducing greenhouse gas emissions. Furthermore, an oversupply of Certified Emissions Reduction has led to plunging prices, hindering withdrawal of the country’s investments.

China is set to actively begin to enforce the carbon emissions trading system in 2015. China has also set up systematic measures to prevent the type of problems seen in the EU’s carbon market. First, the country plans to expand its emissions trading system from the seven pilot areas (including Shenzen) selected for 2013-2015, to all of China from 2015 onward.

Is Australia’s carbon tax sustainable?

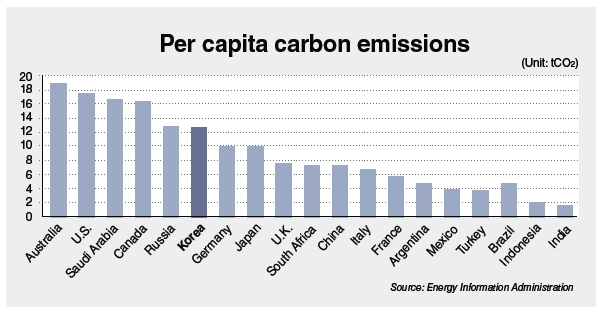

Australia, a signee to the Kyoto Protocol, generates just 1.3 percent of global greenhouse emissions, or 4.3 billion tCO2. However, per capita carbon emissions amount to 19 tCO2, the world’s highest, because the country depends heavily on coal for manufacturing and power.

To this end, in 2012, Australia became the world’s first and only country to impose a fixed-price carbon tax scheme. It called for a tax of $20.52 per tCO2 until 2015 and then a floating tax rate. The opposition Liberal Party, tapping into public and corporate opposition to the additional tax burden, won the Australian general election in September. The Liberal government aims to quickly scrap the carbon tax, and the fate of a 2014 emissions trading plan proposed by the previous administration is uncertain. But if emissions trading starts, the price of emissions would fall to EU levels. Under the trading plan, Australia also would link up with the EU’s carbon market in 2015 to allow its companies to purchase the EU’s emissions rights, which will reduce cost burdens on Australian companies.

Korean situation and its implications

Korea, like China, is one of the world’s top emitters of greenhouse gas and has likewise actively pursued CDM projects but with relatively little effect. Despite investing about $1.9 billion into 86 CDM projects, Korea’s greenhouse gas emissions have risen from 520 million tCO2 in 2007 to 610 million tCO2 in 2011, an annual 4.1 percent increase on average. During the same period, global growth in greenhouse gas emissions was 1.9 percent. In 2011, Korea ranked No. 7 in the world for greenhouse gas emissions, and No. 6 for per capita greenhouse gas emissions at 12.6 tCO2 per person.

Accordingly, Korea in July 2011 has established a target of a 30 percent reduction of global greenhouse gas emissions projected in 2020, the highest level recommended for developing countries. It will implement an emissions trading system in 2015. In order to bridge oversight until 2015, a greenhouse gas and energy target management system is currently being enforced on large-scale greenhouse emitters. In 2012, 586 businesses were eligible, up from 286 in 2010.

It is critical to design a system that can create synergies and promote business competitiveness before the enforcement of the emissions trading system in 2015.

In order to reduce the social and economic burden induced by this system, Korea should carefully benchmark the main carbon markets in the EU, China, the U.S. and Australia. In particular, Korea should pay close attention to China. Like Korea, manufacturing accounts for a large portion of its economy and China is on a similar time schedule for introducing emissions trading.

There is a need to build emissions trading systems that can increase the competitiveness of Korean businesses and effectively respond to climate change. First, since the imbalance of supply and demand in the carbon market can worsen due to economic environment, a flexible allocation system is needed in order to adjust allotments post facto. Second, it is necessary to allow the purchase of overseas CERs or to raise the CER permitted level (which is 10 percent of emissions), and ease the burden on business because excessive reduction targets can cause a rapid increase in the price of rights. Third, Korean businesses’ overseas operations should be included in domestic emissions rights. This can be a way to invigorate the entry of Korean firms overseas. In Japan, if domestic and emerging market firms make one-to-one agreements to reduce emissions, these are recognized as greenhouse gas reductions, thus incentivizing domestic businesses to enter overseas markets. Finally, in order to address uncertainty in the external environment, it will be necessary to establish appropriate contingency plans.

The article was contributed by the Samsung Economic Research Institute. The opinion reflected in the article are SERI’s own. ― Ed.

-

Articles by Korea Herald