Most Popular

-

1

Ador CEO denies allegations, accuses Hybe of mistreating NewJeans

-

2

Medical reform committee kicks off despite boycott from doctors

-

3

10-man S. Korea lose to Indonesia to miss out on Paris Olympic football qualification

-

4

Hybe-Ador feud should have limited effect on Hybe's overall performance: analysts

-

5

DP leader says he will meet Yoon without conditions

-

6

Second Gimpo civil servant found dead, after apologizing for not finishing work

-

7

Over 9,000 hotline calls made by stalking victims in 2023

-

8

[Hello India] Hyundai Motor vows to boost 'clean mobility' in India

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

-

9

Monthly users on local streaming platforms outpace Netflix, Disney+

-

10

US will take steps for three-way engagement on nuclear deterrence with S. Korea, Japan: Campbell

![[Hello India] Hyundai Motor vows to boost 'clean mobility' in India](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/25/20240425050672_0.jpg&u=)

Regulator moves to punish lenders for breaching rules on interest rates

A major disruption is expected to hit the private lending market dominated by Japanese firms as Korea’s financial regulators threaten to suspend leading players for violating rules.

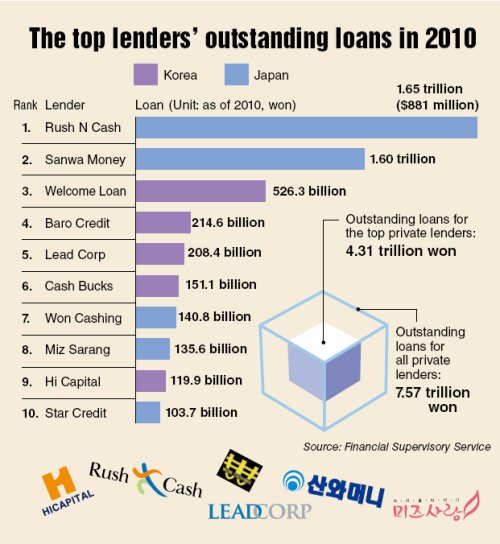

Amid growing public outcry over the high interest rates charged by private lenders, the initial salvo came on Nov. 6 from the Financial Supervisory Service, which confirmed it was considering suspending major lenders including No. 1 player A&P Financial, a Japanese lender known here as Rush N Cash.

The FSS claimed private lenders continued to charge interest rates of 44 to 49 percent and made illegal profits of about 3 billion won in extra interest income even after the maximum rate was lowered to 39 percent in June.

A&P Financial, Sanwa Money, ranked second in the market, and other firms accused of loan abuse have strongly protested the regulator’s move, pledging to take legal action against the envisioned suspension order.

The FSS’s move is part of the Korean government’s efforts to rein in snowballing household debt, which could undercut the broader Korean economy already suffering slowing growth and dwindling orders from crisis-hit Europe.

Money lenders and the FSS are locked in a battle over interpreting and applying the new loan interest ceiling. FSS officials said the companies in question should have applied the new rates when the loan contracts were automatically renewed. Lenders, however, argued they did not receive any specific guideline.

In 2007, the authorities lowered the interest ceiling from 66 percent to 49 percent per year and forced firms to apply the reduced rate to all loans, including those issued before the new rule.

The rule was adjusted last year: Lenders could charge up to 44 percent, down from 49 percent, for loans that are renewed.

The authorities plan to place a six-month suspension order on A&P Financial, Sanwa Money Miz Sarang and One Cashing. But it is not clear if the suspensions will hold, as lenders have twice won legal fights against similar moves by the FSS.

The FSS is putting more pressure on the firms involved, threatening to investigate any private lender that customers claim has violated rules.

There are concerns that a suspension of private lenders would fuel illegal lending, as people with low credit ratings rely on such lenders to borrow legitimately.

The FSS, however, countered that private money lenders had used simplified application procedures to sign up many borrowers with normal credit ratings. People who have trouble getting loans at banks, an FSS official said, could use savings banks or other financial institutions if private lenders are suspended.

The clash between the authorities and private money lenders is expected to make local customers more nervous following the turmoil resulting from the business suspension of savings banks.

The four private lenders accused of irregularities command 1.15 million customers, accounting for 40 percent in combined market share. A business suspension order would force them to stop extending new or additional loans.

The public image of such firms is also likely to suffer. About 20 private money lenders backed up by Japanese capital dominate the local market after witnessing rapid growth over the past decade.

According to the FSS, Japan-based private money lenders had a loan balance of 3.75 trillion won, controlling about 50 percent of the total market valued at 7.5 trillion won as of December last year.

Japanese firms’ dramatic growth is largely because they secure capital at a lower rate ― usually 7-8 percent per year in Japan ― and carry over the money to the Korean market, whereas their Korean rivals have to pay an annual interest of at least 12 percent to secure base capital.

Lenders of Japanese capital, however, have been under fire for charging the maximum interest rate on virtually all customers regardless of their personal credit ratings.

By Yang Sung-jin (insight@heraldcorp.com)

A major disruption is expected to hit the private lending market dominated by Japanese firms as Korea’s financial regulators threaten to suspend leading players for violating rules.

Amid growing public outcry over the high interest rates charged by private lenders, the initial salvo came on Nov. 6 from the Financial Supervisory Service, which confirmed it was considering suspending major lenders including No. 1 player A&P Financial, a Japanese lender known here as Rush N Cash.

The FSS claimed private lenders continued to charge interest rates of 44 to 49 percent and made illegal profits of about 3 billion won in extra interest income even after the maximum rate was lowered to 39 percent in June.

A&P Financial, Sanwa Money, ranked second in the market, and other firms accused of loan abuse have strongly protested the regulator’s move, pledging to take legal action against the envisioned suspension order.

The FSS’s move is part of the Korean government’s efforts to rein in snowballing household debt, which could undercut the broader Korean economy already suffering slowing growth and dwindling orders from crisis-hit Europe.

Money lenders and the FSS are locked in a battle over interpreting and applying the new loan interest ceiling. FSS officials said the companies in question should have applied the new rates when the loan contracts were automatically renewed. Lenders, however, argued they did not receive any specific guideline.

In 2007, the authorities lowered the interest ceiling from 66 percent to 49 percent per year and forced firms to apply the reduced rate to all loans, including those issued before the new rule.

The rule was adjusted last year: Lenders could charge up to 44 percent, down from 49 percent, for loans that are renewed.

The authorities plan to place a six-month suspension order on A&P Financial, Sanwa Money Miz Sarang and One Cashing. But it is not clear if the suspensions will hold, as lenders have twice won legal fights against similar moves by the FSS.

The FSS is putting more pressure on the firms involved, threatening to investigate any private lender that customers claim has violated rules.

There are concerns that a suspension of private lenders would fuel illegal lending, as people with low credit ratings rely on such lenders to borrow legitimately.

The FSS, however, countered that private money lenders had used simplified application procedures to sign up many borrowers with normal credit ratings. People who have trouble getting loans at banks, an FSS official said, could use savings banks or other financial institutions if private lenders are suspended.

The clash between the authorities and private money lenders is expected to make local customers more nervous following the turmoil resulting from the business suspension of savings banks.

The four private lenders accused of irregularities command 1.15 million customers, accounting for 40 percent in combined market share. A business suspension order would force them to stop extending new or additional loans.

The public image of such firms is also likely to suffer. About 20 private money lenders backed up by Japanese capital dominate the local market after witnessing rapid growth over the past decade.

According to the FSS, Japan-based private money lenders had a loan balance of 3.75 trillion won, controlling about 50 percent of the total market valued at 7.5 trillion won as of December last year.

Japanese firms’ dramatic growth is largely because they secure capital at a lower rate ― usually 7-8 percent per year in Japan ― and carry over the money to the Korean market, whereas their Korean rivals have to pay an annual interest of at least 12 percent to secure base capital.

Lenders of Japanese capital, however, have been under fire for charging the maximum interest rate on virtually all customers regardless of their personal credit ratings.

By Yang Sung-jin (insight@heraldcorp.com)

-

Articles by Korea Herald