Most Popular

-

6

[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs

![[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/18/20240418050645_0.jpg&u=20240419100350)

-

7

North Korea removes streetlights along cross-border roads with South

-

8

Russia's denial of entry of S. Korean national unrelated to bilateral ties: Seoul official

-

9

S. Korea votes in favor of Palestinian bid for UN membership

-

10

Farming households dip below 1m for first time in 2023

![[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/18/20240418050645_0.jpg&u=20240419100350)

[ANALYST REPORT] Hankook Tire: Weak raw material prices lead to strong results

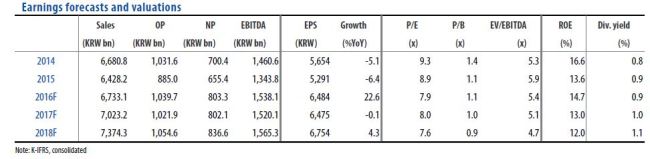

By 박한나Published : Aug. 18, 2016 - 16:38

1) Investment highlights

- 2Q16 output and sales narrowly beat our forecasts but lower-than-expected raw material costs combined with an improving product mix (e.g., robust sales of UHPT) drove operating profit much higher than the consensus and our estimates.

- The domestic market remains sluggish, but in China, the pace of sales decline is slowing. Growth in European and North American sales are still upbeat. With the growth in demand slowing, price competition will likely continue for a bit longer. The recent sharp appreciation of the KRW against the EUR and USD is burdensome for 2H16 earnings.

- The price of natural rubber has finally pulled out of its protracted decline. Its surge since February should have a positive impact on earnings from 3Q16. The 2Q16 operating margin of 18% was the highest since the introduction of the consolidated accounting system, but we expect it to come off the peak in 2H16.

- We slightly raise our 2H16 and 2017 earnings forecasts and lift our target price to KRW58,000.

However, we maintain our Marketperform rating in light of the demanding valuation.

2) Major issues and earnings outlook

- 2Q16 sales came to KRW1.73tn (+6.6% YoY) and global output 25.22mn units (+4.1% YoY). Both were in line with expectations. Sales were driven by growth in volume as well as favorable FX and product mix (e.g., UHPT). Operating profit was 28.1% higher than our estimate on a steeper-thanexpected decline in raw material costs.

- Sales in North America and Europe jumped 18.9% and 16.4% YoY, respectively, thanks to growing volumes, a better product mix, and favorable FX. However, the domestic market saw seven consecutive quarters of decline YoY. Meanwhile, in China, the pace of sales decline appears to be slowing.

- Raw material cost fell to USD1,458/ton (-12.1% YoY, -2.3% QoQ) but we expect it to move upward given the sharp rise in the price of natural rubber since February.

3) Share price outlook and valuation

- We nudge up our target price to KRW58,000, applying our target P/E of 9.7x to the average EPS of 3Q16-2Q17F (the average P/E of eight global peers). We keep our rating unchanged at Marketperform on the limited valuation merit vs. global peers and concerns over potential margin erosion in 2H16.

Source: HMC Investment Securities

- 2Q16 output and sales narrowly beat our forecasts but lower-than-expected raw material costs combined with an improving product mix (e.g., robust sales of UHPT) drove operating profit much higher than the consensus and our estimates.

- The domestic market remains sluggish, but in China, the pace of sales decline is slowing. Growth in European and North American sales are still upbeat. With the growth in demand slowing, price competition will likely continue for a bit longer. The recent sharp appreciation of the KRW against the EUR and USD is burdensome for 2H16 earnings.

- The price of natural rubber has finally pulled out of its protracted decline. Its surge since February should have a positive impact on earnings from 3Q16. The 2Q16 operating margin of 18% was the highest since the introduction of the consolidated accounting system, but we expect it to come off the peak in 2H16.

- We slightly raise our 2H16 and 2017 earnings forecasts and lift our target price to KRW58,000.

However, we maintain our Marketperform rating in light of the demanding valuation.

2) Major issues and earnings outlook

- 2Q16 sales came to KRW1.73tn (+6.6% YoY) and global output 25.22mn units (+4.1% YoY). Both were in line with expectations. Sales were driven by growth in volume as well as favorable FX and product mix (e.g., UHPT). Operating profit was 28.1% higher than our estimate on a steeper-thanexpected decline in raw material costs.

- Sales in North America and Europe jumped 18.9% and 16.4% YoY, respectively, thanks to growing volumes, a better product mix, and favorable FX. However, the domestic market saw seven consecutive quarters of decline YoY. Meanwhile, in China, the pace of sales decline appears to be slowing.

- Raw material cost fell to USD1,458/ton (-12.1% YoY, -2.3% QoQ) but we expect it to move upward given the sharp rise in the price of natural rubber since February.

3) Share price outlook and valuation

- We nudge up our target price to KRW58,000, applying our target P/E of 9.7x to the average EPS of 3Q16-2Q17F (the average P/E of eight global peers). We keep our rating unchanged at Marketperform on the limited valuation merit vs. global peers and concerns over potential margin erosion in 2H16.

Source: HMC Investment Securities

![[From the Scene] Monks, Buddhists hail return of remains of Buddhas](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=652&simg=/content/image/2024/04/19/20240419050617_0.jpg&u=20240419175937)

![[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=652&simg=/content/image/2024/04/18/20240418050645_0.jpg&u=20240419100350)

![[Today’s K-pop] Illit drops debut single remix](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=642&simg=/content/image/2024/04/19/20240419050612_0.jpg&u=)