Most Popular

-

1

[Exclusive] Korean military set to ban iPhones over 'security' concerns

![[Exclusive] Korean military set to ban iPhones over 'security' concerns](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/23/20240423050599_0.jpg&u=20240423183955)

-

2

Korean, Romanian leaders discuss defense tech, nuclear energy

-

3

[Graphic News] 77% of young Koreans still financially dependent

![[Graphic News] 77% of young Koreans still financially dependent](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/22/20240422050762_0.gif&u=)

-

4

S. Korea calls on Japan to confront history amid Yasukuni Shrine visit

-

5

Yoon’s jailed mother-in-law excluded from latest parole list

![[Exclusive] Korean military set to ban iPhones over 'security' concerns](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/23/20240423050599_0.jpg&u=20240423183955)

![[Graphic News] 77% of young Koreans still financially dependent](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/22/20240422050762_0.gif&u=)

-

6

Hybe and Min Hee-jin, CEO of Hybe sublabel Ador, lock horns

-

7

[Pressure points] Leggings in public: Fashion statement or social faux pas?

![[Pressure points] Leggings in public: Fashion statement or social faux pas?](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/23/20240423050669_0.jpg&u=)

-

8

Yoo Jae-suk, Yoo Yeon-seok team up in 'Whenever Possible'

-

9

Aging population to drive down Korea's housing prices from 2040: experts

-

10

North Korea holds drills simulating nuclear counterattack against enemy

![[Pressure points] Leggings in public: Fashion statement or social faux pas?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/23/20240423050669_0.jpg&u=)

[THE INVESTOR] MBK Partners, Korea’s most successful buyout fund, is gearing up for its biggest fundraising push amid intensifying competition from global private-equity giants and fast-emerging regional rivals.

It is currently premarketing its fourth fund, aiming for $4 billion, a source familiar with the matter said, with actual fundraising expected to begin later this year.

It is currently premarketing its fourth fund, aiming for $4 billion, a source familiar with the matter said, with actual fundraising expected to begin later this year.

If successful, MBK’s new fund would rank among the biggest set up in Asia in recent years by such global names KKR, Baring and Carlyle and Asia-focused emerging player RRJ Capital.

Tougher competition -- both in deal making and fundraising -- is a key challenge facing MBK, its founder and chairman Michael Byung-ju Kim noted in his letter to investors wrapping the year 2015.

“Our competitors are returning to Japan and especially Korea to ride the corporate restructuring wave, private equity’s version of hallyu,” he wrote.

US investment behemoth KKR, which holds a fundraising record in Asia with its $6 billion fund set up in 2013, aims to attract $7 billion with a new fund to launch this year.

Hong Kong-based RRJ, established in 2011, last year rose to the No. 2 spot with the launch of a $4.5 billion corporate buyout fund.

“The success of (MBK’s) fundraising will hinge on international investors,” said a local PE industry insider. “The maximum that can be raised locally is believed to be around $1 billion,” he said.

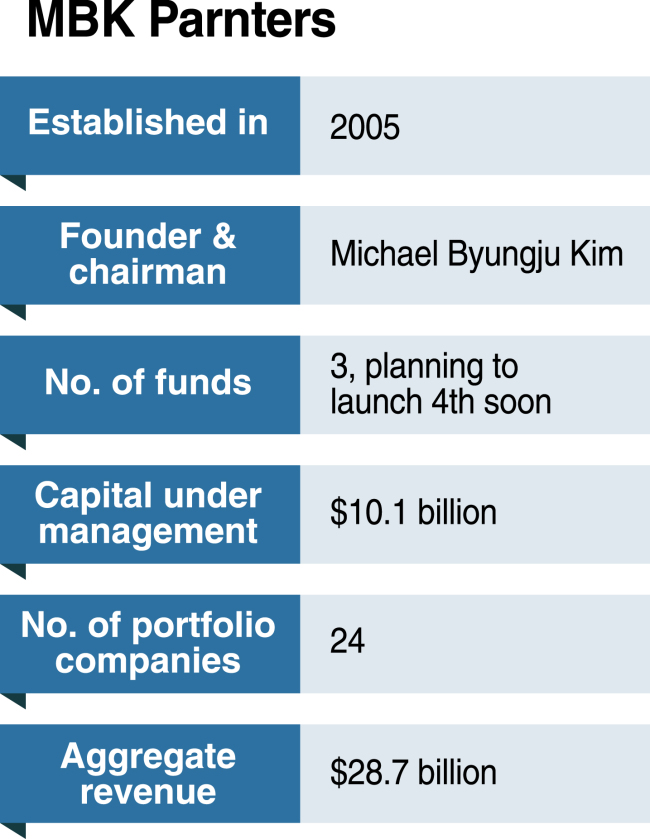

Started in 2005 with a clear focus on China, Korea and Japan, MBK made its mark in the global PE industry last year when it came out as a surprise winner of the hotly-contested race to buy Tesco’s Korean supermarket chain. The $6.1 billion Homeplus deal is, to this day, one of the region’s biggest private-equity led buyouts.

A $4 billion new fund would reconfirm the Korean fund house’s status among the region’s private-equity big league, local watchers said.

Troubled exits in Korea

The new fundraising push comes as MBK has executed nearly 70 percent of the dry powder in its third and youngest fund set up in 2013 with $2.7 billion.

Managing a total of over $10 billion in three funds, the firm has made 24 investments, 17 of which it has already exited or partially exited.

A local report said MBK outsmarted KKR and other regional rivals with total returns of $3.3 billion between June 2014 and this year. Kim, the MBK chairman, has also revealed that the year 2015 was a record year of investment exits with proceeds totaling $2.7 billion.

Despite the impressive overall performance, MBK is facing difficulty in exiting, or even potential losses in, some of its Korean investments.

C&M, renamed D’Live, and Young Hwa Construction & Engineering are sure to become major stains on the firm’s otherwise-impressive investment track record.

MBK’s local reputation was dented last year when the vehicle it set up for the acquisition of the Korean cable-TV operator C&M narrowly averted a default on loans it took out for the deal.

The value of C&M is believed to have fallen below $2 billion, what the MBK-led consortium paid for its purchase in 2008.

The MBK’s first fund, which executed the investment, however, has made solid proceeds in its other portfolio investments, enough to cover the potential C&M losses.

MBK is focusing on improving C&M’s corporate value for now and will consider a sale two or three years later, a source familiar with the matter said.

As for Young Hwa E&C, an investment loss seems inevitable.

The firm, currently under court receivership, is in the process of finding a new owner, with two bidders having expressed their interest in the steel and metal structures maker. The price, if any, would fall significantly below that the 100 billion won that MBK paid in 2009, as the court put the firm’s value as a going concern at about 65 billion won and at 50 billion won when it is liquidated.

Coway is another headache for MBK.

Last month, the water purifier maker and rental firm said in a regulatory filing that its largest shareholder -- Coway Holdings which is 30.9 percent owned by MBK -- has “decided to suspend its plan to sell shares in the firm, believing the shares are undervalued.”

The deferral comes after Coway was found to have mechanical defects in water purifiers that taint water with powdered nickel. Last month, after a fact-finding investigation, the Korean government ordered a recall of all defective products.

The nickel scandal put a brake on MBK’s plan to realize a handsome profit on its 1.2 trillion won investment in the firm. Local reports said MBK was looking at a price of over 3 trillion won for its 30.9 percent stake in the firm.

MBK is nearing an exit from ING Life Insurance Korea, currently in negotiations with at least four investors from China and Hong Kong -- JD Capital, China Taiping Insurance, Anbang Insurance and Fosun.

It said in a press conference last month that the buyer will be decided before this winter.

In December 2013, it bought 100 percent of ING Life for 1.8 trillion won. Local reports say MBK hopes for a price of about 3 trillion won.

By Lee Sun-young/The Korea Herald (milaya@heraldcorp.com)

This is the third in a series of articles looking into Korea’s private equity market and its key players. -- Ed.