Most Popular

-

1

K-pop group's manager dismissed for setting up spycam in theater dressing room

-

2

Contentious grain bill put directly to plenary meeting for vote

-

3

Why is Apple Pay struggling to get purchase in Korea?

-

4

Will tug-of-war between doctors, government end soon?

-

5

Climate impacts set to cut 2050 global GDP by nearly a fifth

-

6

Trilateral talks acknowledge ‘serious’ slumps of won, yen

-

7

[Today’s K-pop] BTS pop-up event to come to Seoul

![[Today’s K-pop] BTS pop-up event to come to Seoul](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/17/20240417050734_0.jpg&u=)

-

8

Yoon's approval rating plunges to all-time low

-

9

[Graphic News] More Koreans say they plan long-distance trips this year

![[Graphic News] More Koreans say they plan long-distance trips this year](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/17/20240417050828_0.gif&u=)

-

10

Mother of student activist, whose death sparked pro-democracy movement, dies

![[Today’s K-pop] BTS pop-up event to come to Seoul](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/17/20240417050734_0.jpg&u=)

![[Graphic News] More Koreans say they plan long-distance trips this year](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/17/20240417050828_0.gif&u=)

[ANALYST REPORT] Samsung Heavy Industries: Rights offering decided; TP cut likely less steep than expected

By 박한나Published : Aug. 23, 2016 - 13:21

Rights offering

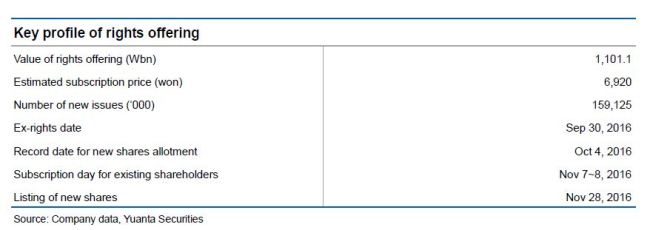

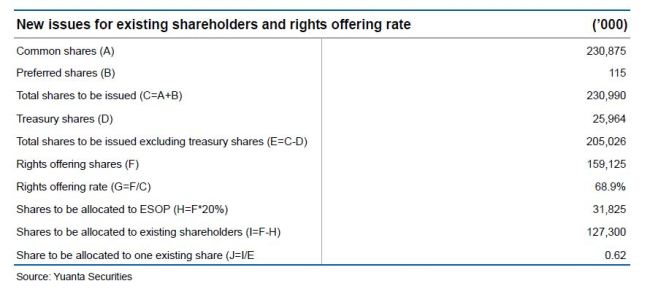

On Aug 19, Samsung Heavy Industries decided to conduct a W1.1tn of rights offering. Offering rights to existing shareholders to purchase 159.12mn shares at the subscription price of W6,920, the company will make the offering to the general public. The ex-right date will be Sep. 30 and the new shares will be listed on Nov 28. Currently, Samsung affiliates and related parties hold a 24% stake, with Samsung Electronics 17.62%, Samsung Life Insurance 3.38%, and Samsung Electro-Mechanics 2.39%. Unlike for Samsung Engineering, Samsung Group’s owner family did not pledge to purchase forfeited shares.

Likely to help ease liquidity issue

Samsung Heavy is now suffering a severe liquidity problem. In 1H16, operating cash flow was -W891.9bn, and debts to mature from Jul 2016 to Jun 2017 amount to W3.8tn (including W2.86tn of short-term debt, W909.7bn of the current portion of long-term debt, W399.6bn of debentures to mature in Feb 2017). According to reports, creditors including KDB will extend maturity by three months, not 12 months, to control risks.

However, if the rights offering succeeds, the situation will improve significantly. As cash equivalents will rise to about W2.0tn (W910.0bn at end-1H16 + proceeds from rights offering of W1.1tn), the company’s finances will improve, which should make creditors much more flexible in extending loan maturity. Our outlook for 2017 operating cash flow is not bad for two reasons.

First, the number of vessel deliveries (excluding drillships) is set to rise from 31 in 2016E to 42 in 2017E, while the contract value will likely rise 25% from $4.75bn to $5.93tn and the delivery installment will also increase that much. If the company actually delivers some of the four drillships set to be delivered in 2017, cash flow will improve. Second, fewer vessel constructions in 2017 due to weak new orders in 2016 will be positive in terms of cash flow. In “heavy-tail”payment schemes, demand for funds increases when ship construction increases.

However, even after the rights offering, debt-to-equity should still stand at 200%, and if the offshore division sees more losses, the liquidity issue will worsen. The fundamental answer to the liquidity issue is a market turnaround and recovery of new orders. However, the rights offering should give the company more than a year to endure the current situation.

Shares to be diluted but fair valuations may be revised up

The downward revision to our target price from the rights offering may not be as steep as expected. BPS should decline due to share dilution, but fair P/B could increase if the company overcomes the liquidity crisis backed by the rights offering and succeeds in turning to profit in 2H16. For example, if P/B rises from 0.4x now to 0.6x, the same level as Hyundai Heavy, fair

price should be W9,700 (based on BPS of W16,243). However, whether shares increase further than that should depend on oil prices and market conditions. We will revise down our target price after the subscription price is finalized.

Source: Yuanta Securities

On Aug 19, Samsung Heavy Industries decided to conduct a W1.1tn of rights offering. Offering rights to existing shareholders to purchase 159.12mn shares at the subscription price of W6,920, the company will make the offering to the general public. The ex-right date will be Sep. 30 and the new shares will be listed on Nov 28. Currently, Samsung affiliates and related parties hold a 24% stake, with Samsung Electronics 17.62%, Samsung Life Insurance 3.38%, and Samsung Electro-Mechanics 2.39%. Unlike for Samsung Engineering, Samsung Group’s owner family did not pledge to purchase forfeited shares.

Likely to help ease liquidity issue

Samsung Heavy is now suffering a severe liquidity problem. In 1H16, operating cash flow was -W891.9bn, and debts to mature from Jul 2016 to Jun 2017 amount to W3.8tn (including W2.86tn of short-term debt, W909.7bn of the current portion of long-term debt, W399.6bn of debentures to mature in Feb 2017). According to reports, creditors including KDB will extend maturity by three months, not 12 months, to control risks.

However, if the rights offering succeeds, the situation will improve significantly. As cash equivalents will rise to about W2.0tn (W910.0bn at end-1H16 + proceeds from rights offering of W1.1tn), the company’s finances will improve, which should make creditors much more flexible in extending loan maturity. Our outlook for 2017 operating cash flow is not bad for two reasons.

First, the number of vessel deliveries (excluding drillships) is set to rise from 31 in 2016E to 42 in 2017E, while the contract value will likely rise 25% from $4.75bn to $5.93tn and the delivery installment will also increase that much. If the company actually delivers some of the four drillships set to be delivered in 2017, cash flow will improve. Second, fewer vessel constructions in 2017 due to weak new orders in 2016 will be positive in terms of cash flow. In “heavy-tail”payment schemes, demand for funds increases when ship construction increases.

However, even after the rights offering, debt-to-equity should still stand at 200%, and if the offshore division sees more losses, the liquidity issue will worsen. The fundamental answer to the liquidity issue is a market turnaround and recovery of new orders. However, the rights offering should give the company more than a year to endure the current situation.

Shares to be diluted but fair valuations may be revised up

The downward revision to our target price from the rights offering may not be as steep as expected. BPS should decline due to share dilution, but fair P/B could increase if the company overcomes the liquidity crisis backed by the rights offering and succeeds in turning to profit in 2H16. For example, if P/B rises from 0.4x now to 0.6x, the same level as Hyundai Heavy, fair

price should be W9,700 (based on BPS of W16,243). However, whether shares increase further than that should depend on oil prices and market conditions. We will revise down our target price after the subscription price is finalized.

Source: Yuanta Securities

![[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=652&simg=/content/image/2024/04/18/20240418050645_0.jpg&u=20240419100350)