Most Popular

-

6

[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs

![[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/18/20240418050645_0.jpg&u=20240419100350)

-

7

North Korea removes streetlights along cross-border roads with South

-

8

Russia's denial of entry of S. Korean national unrelated to bilateral ties: Seoul official

-

9

S. Korea votes in favor of Palestinian bid for UN membership

-

10

Farming households dip below 1m for first time in 2023

![[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/18/20240418050645_0.jpg&u=20240419100350)

[ANALYST REPORT] Celltrion: Expect healthy 3Q16 share price momentum

By Korea HeraldPublished : July 1, 2016 - 16:20

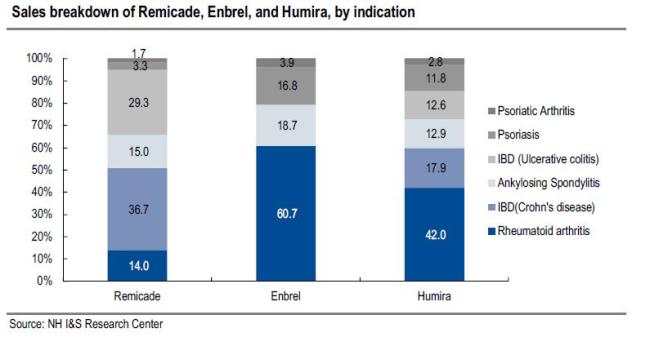

Celltrion’s sales and profit should normalize from 2Q16. Looking at 2H16, we suggest that investors focus on: 1) the start of supply (from 3Q16) of Celltrion Healthcare’s Remsima to Pfizer; 2) expected approvals for Celtrion’s Rituxan and Herceptin biosimilars; 3) a planned IPO for Celltrion Healthcare; and 4) new disclosure rules for short-selling balances.

2Q16 preview: Earnings normalizing; COGS-to-sales ratio and SG&A-to-sales ratio stabilizing

2Q16 preview: Earnings normalizing; COGS-to-sales ratio and SG&A-to-sales ratio stabilizing

We expect Celltrion to register non-consolidated 2Q16 sales of W157.2bn (up 5.5% y-y), operating profit of W77.9bn (down 2.3% y-y), and net profit of W64.2bn (up 21.6% y-y), with sales and operating profit missing consensus by 3.7% and 8.7%, respectively, but new profit topping by 3.3%.

On Jun 22, 2016, Celltrion announced that it has signed a supply contract (products: W145.6bn; services: W10.1bn) with Celltrion Healthcare. Of note, Celltrion’s 1Q16 results missed consensus on less-than-expected utilization rate at its production facilities and higher R&D expenditure. However, backed by stabilizing COGS-to-sales and SG&A-to-sales ratios, we expect Celltrion to post a 2Q16 operating margin of 49.6% (down 3.9%p y-y).

Celltrion’s next focal points

Celltrion received US FDA approval for Remsima on Apr 5, 2016. According to the information exchange requirements under the Public Health Service Act 351 (i) (which is part of the BPCIA’s patent dispute resolution scheme), biosimilar players must notify the original biologics company not later than 180 days before the start of planned initial commercial marketing activities for a new related product.

With Remsima set to be launched in the US in October, we expect Celltrion Healthcare to supply the first batch to Pfizer in 3Q16.

According to media reports, the estimated size of the first batch (indicator of Remsima’s potential for success in the US market) will be W200bn~W400bn. On Jun 23, senior Republican Senator John McCain proposed the ‘Price Relief, Innovation and Competition for Essential Drugs (PRICED) Act’. The act would cut the exclusivity period on biologics from 12 years to 7 years.

If PRICED comes into being, the US health insurance budget would in turn be reduced by an estimated US$680mn over the next 10 years, a development which would bode well for biosimilar players.

Having already applied for Investigational New Drug (IND) status from the EU EMA for its ‘Herceptin’ biosimilar ‘Herzuma Celltrion’, Celltrion plans to apply for US FDA IND status for the product in 1Q17. Its Rituxan biosimilar Truxima should receive EU EMA approval in 4Q16 and US FDA approval in 1Q17.

Should Celltrion Healthcare supply the first batch of Remsima in 3Q16 as expected, Celltrion Healthcare is to then apply for screening in preparation for going public on the Kosdaq. If Celltrion Healthcare is listed by the end of 2016, Celltrion’s related accounting issue woes should be resolved.

In Jun 30, Korea government enforced disclosure of short-selling balances. The new disclosure rules are applicable to investors whose short-selling of a particular listed company is worth W1.0bn or more.

In addition, irrespective of worth, investors whose short-selling balance sheet exceeds 0.5 percent of a particular company’s total stocks issued must also go public. The short-sellingto- total market capital ratio for Celltrion is 20.7%. With the new disclosure rule, we expect short-selling pattern on the firm’s shares to change.

Source: NH Investment & Securities http://www.nhfngroup.com/Eng/affiliates/subsidiary_4.aspx

-

Articles by Korea Herald

![[From the Scene] Monks, Buddhists hail return of remains of Buddhas](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=652&simg=/content/image/2024/04/19/20240419050617_0.jpg&u=20240419175937)

![[KH Explains] Hyundai's full hybrid edge to pay off amid slow transition to pure EVs](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=652&simg=/content/image/2024/04/18/20240418050645_0.jpg&u=20240419100350)

![[Today’s K-pop] Illit drops debut single remix](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=642&simg=/content/image/2024/04/19/20240419050612_0.jpg&u=)