Most Popular

-

6

[KH Explains] How should Korea adjust its trade defenses against Chinese EVs?

![[KH Explains] How should Korea adjust its trade defenses against Chinese EVs?](//res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/15/20240415050562_0.jpg&u=20240415144419)

-

7

BTS' Jungkook creates Instagram account for his dog

-

8

Korea braces for blows from Middle East conflict

-

9

Seoul says will cut power to porn festival planned on Han River

-

10

Recording of boss cursing in office ruled legal

![[KH Explains] How should Korea adjust its trade defenses against Chinese EVs?](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/04/15/20240415050562_0.jpg&u=20240415144419)

2Q estimates: sales of W3.76tr (+2.1% QoQ), OP of W445bn (-21.6% QoQ) Rebounding indicators, earnings to improve QoQ in 3Q ¨

Retain BUY for target price of W38,000

Retain BUY for target price of W38,000

2Q estimates: sales W3.76tr (+2.1% QoQ), operating profit W445bn (-21.6% QoQ)

SK Hynix is forecast to post 2Q sales of W3.76tr (+2.1% QoQ, -18.9% YoY) and operating profit of W445bn (-21.6% QoQ, -67.7% YoY). We expect bit growth of 13% and ASP drop of 10%. Earnings should bottom out in 2Q. We expect operating profit of W549bn (+23.5% QoQ) for 3Q and W520bn (-5.3% QoQ) for 4Q.

Rebounding indicators, earnings to improve QoQ in 3Q

In an earlier report (title: Passing the bottom of the downcycle), we expected a decline in the oversupply ratio (3% in 1H → 1.5% in 2H, 2.2% for 2016) in 2H16 based on: 1) pick-up in demand from BRIC countries, 2) mild effect of slowing growth (52% in 2015 → 35% in 2016) on increased mobile DRAM requirements and 3) slower capacity expansion for 20nm class DRAM vs. Samsung Electronics (ramp-up of 40K wpm, output share of 20nm class: 80%) last year. We have been seeing these three factors in 2Q.

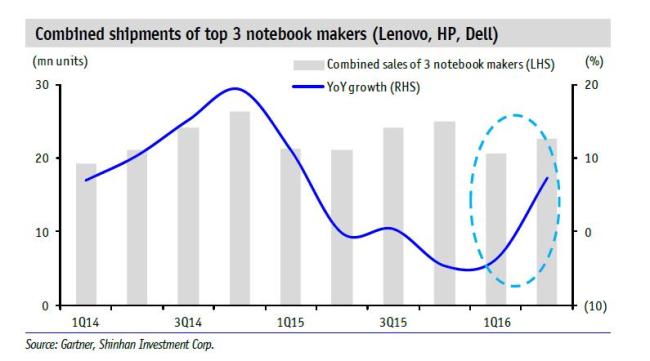

1) Cyclical components of OECD Composite Leading Indicators continue to move higher for all BRIC economics as the figure for China showed a rebound from March. The top three notebook makers expanded their shipments by 30% MoM in May, spurring expectations for YoY growth in 2Q. This should help clear PC DRAM inventories of SK Hynix (PC DRAM bit growth to be negative in 2Q).

2) Mobile phones are being upgraded for both high-end (3GB→4GB, release of new model with 6GB) and low-end models (1GB→2GB). The iPhone 7S Plus is expected to have greater memory (2GB→3GB).

3) SK Hynix is expected to boost the share of 20nm class DRAM production to 40% by end-2016 (8% in 2Q16, faster ramp-up in 3Q) and shift its focus to DDR4, while Micron will likely raise the share of 20nm to 45% and concentrate on DDR3.

Retain BUY for target price of W38,000

Spot price of PC DRAM rose 11.9% and mobile DRAM has not plunged, contrary to concerns. The recent surge in orders from Chinese smartphone makers has yet to translate to sales; thus, orders could drop in 3Q16. However, 20nm shipments for new iPhones should grow sharply QoQ. We retain our target price of W38,000.

Source: Shinhan Investment www.shinhaninvest.com/eng

-

Articles by Korea Herald

![[Today’s K-pop] Stray Kids to return soon: report](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=642&simg=/content/image/2024/04/16/20240416050713_0.jpg&u=)